It’s the IRS to the rescue! Really.

The government agency has come through for those with retirement savings. Within one week in late June, the IRS expanded the relief Congress provided in the CARES Act, releasing guidance for returning unwanted required minimum distributions and expanding coronavirus-related distribution (CRD) provisions so that more U.S. taxpayers will qualify.

The happy result is that financial advisors are now in a position to help clients take advantage of the enhanced relief. Here are actionable takeaways from both IRS rulings.

Unwanted RMDs can now be undone

Even though the CARES Act waived all RMDs due in 2020, many savers had already taken our part or all of their RMDs earlier in the year before they knew about the waiver.

They then wanted to return those unwanted RMDs by rolling those funds back to their IRAs or company plans and eliminating the tax bill. But those efforts ran up against strict rollover rules.

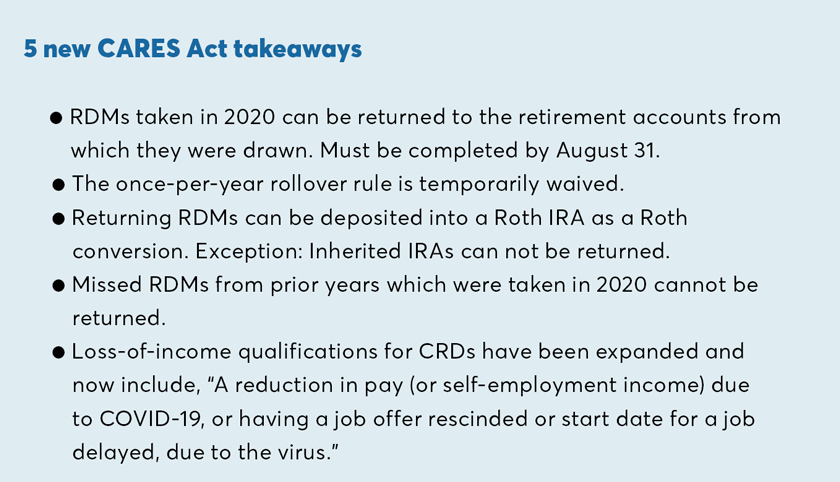

But with IRS Notice 2020-51, released June 23, the IRS provided unprecedented blanket relief for most unwanted RMDs. In this one-off special, the ruling allows that RMDs taken to date in 2020 be returned (rolled back over) to retirement accounts. The agency also waived the once-per-year rollover rule and allowed non-spouse IRA beneficiaries to return unwanted RMDs. Despite the fact that both of these actions are contrary to the tax law, the IRS is allowing these returns as repayments.

Note however, that the relief (the ability to return the unwanted RMDs) only applies to the amount of the RMD withdrawn — and only if done by Aug. 31. After that time, all the regular rollover rules return.

For those who otherwise would not have been able to return the unwanted RMDs due to the once-per-year rule or because they were an IRA beneficiary, the repayment must go to the same account the funds were originally withdrawn from. However, beneficiaries of company plans, like 401(k)s, cannot return their unwanted RMDs.

The temporary waiver of the once-per-year rule also solves the problem of clients who have multiple RMDs, i.e. some who were taking monthly RMDs and were only able to return one of them. Under this new IRS guidance, they can, if they wish, return all of those RMDs — but again, if done by Aug. 31.

Advisors have asked me if the return of the unwanted RMDs could go to a Roth IRA as a Roth conversion. They can — except for IRA beneficiaries who cannot convert an inherited IRA to an inherited Roth IRA. The Roth conversion, of course, would be taxable and would have to be done by Aug. 31 unless the RMDs are still within a 60-day window. The once-per-year rule does not apply to Roth conversions, which is why an unwanted IRA RMD does not have to go back to an IRA.

On the other hand, if a 2020 RMD was already converted to a Roth IRA, that cannot be undone even under this relief, because a Roth conversion cannot be recharacterized.

Are 2019 RMDs eligible?

If a client turned age 70 ½ in 2019, they were still subject to the pre-SECURE Act rules and could not delay RMDs until reaching age 72. Thus, their required beginning date was still April 1, 2020.

The good news, however, is that any part of their 2019 RMD that was not taken in 2019 was waived under the CARES Act. In this hypothetical client’s case, the first two RMDs (2019 and 2020) are waived. If they had taken all or any part of either of those RMDs in 2020, they can return them by Aug. 31.

However, missed RMDs for prior years that were made up in 2020 cannot be returned as the CARES Act only waives RMDs that were originally due in 2020. Those with a first-year RMD for 2019 are covered because that first RMD was not due until April 1.

Year-of-death RMDs

Can a 2020 RMD taken by an IRA owner who died later in 2020 be returned?

Unclear, as the IRS relief does not directly address this situation. The relief is very broad, and it could be argued a beneficiary repaying an RMD taken by the IRA owner would be included. But even if this were permitted, it could have income or estate tax planning ramifications so this should be evaluated before returning an unwanted RMD for a deceased person.

Ed Slott & Co

For example, for income tax purposes, it might pay to keep that RMD income on the decedent’s final tax return if the tax might be lower, say, due to heavy medical expenses that could offset the tax bill. For estate planning, returning an RMD could change a beneficiary’s share. There also may be administrative challenges to returning an unwanted RMD to the IRA of a deceased person. Financial institutions will probably want legal clearance before allowing this.

How about non-RMD rollovers?

Sorry. The extended deadline does not apply to 60-day rollovers of funds that are not unwanted 2020 RMDs. There was relief back in April that included those rollovers but that deadline is July 15. For example, if an IRA owner withdrew non-RMD funds in February, they received an extension until July 15 to complete that rollover, however there was no relief from the once-per-year rule and January 2020 distributions were also excluded. The Aug. 31 extension can only be used for returning unwanted RMDs.

Really good news: More clients now qualify for CRD relief

On June 19, just a few days before it released the RMD relief, the IRS issued IRS Notice 2020-50 allowing more people to qualify for CRDs and adding new qualifying categories to the existing loss-of-income qualifications.

In addition to the original CARES Act qualifications (adverse financial consequences due being quarantined, furloughed, or laid off, or having work hours reduced due to COVID-19 or being unable to work due to lack of childcare due to the virus, or due to the closing or reducing of hours of a business owned or operated by the individual due to the disease), the IRS Notice added these factors to the list: A reduction in pay (or self-employment income) due to COVID-19, or having a job offer rescinded or start date for a job delayed, due to the virus.

The individual will qualify for a CRD as an affected person if any of the above loss-of-income factors applies to their spouse or a member of the household, meaning “someone who shares the individual’s principal residence.”

This could include a child, any other relative, a friend, partner or roommate. For example, if the individual is not sick and suffers no loss of income, but her roommate loses her job and now cannot pay her share of the rent forcing the individual to have to come up with the shortfall to avoid eviction, then that individual now qualifies for a CRD, even though she is not sick or has not lost work income herself.

CRD repayments

CRD income can be spread over three years but if any of those funds can be repaid within three years, the taxes paid can be refunded by filing an amended tax return. The IRS Notice states that an amended tax return will not be required if the CRD funds are repaid by the due date of the tax return that includes the CRD income (plus extensions). In that case, the CRD income does not have to be included on the tax return for that year.

Advisors should be aware of these expanded relief provisions and identify clients who may benefit from them. There may be some clients who could not benefit before these two IRS notices were issued, but now do qualify.

Leave a Reply