Despite absorbing a double-digit hit to its bottom line, LPL Financial reached record levels of client assets and financial advisors with potential new growth areas on the horizon.

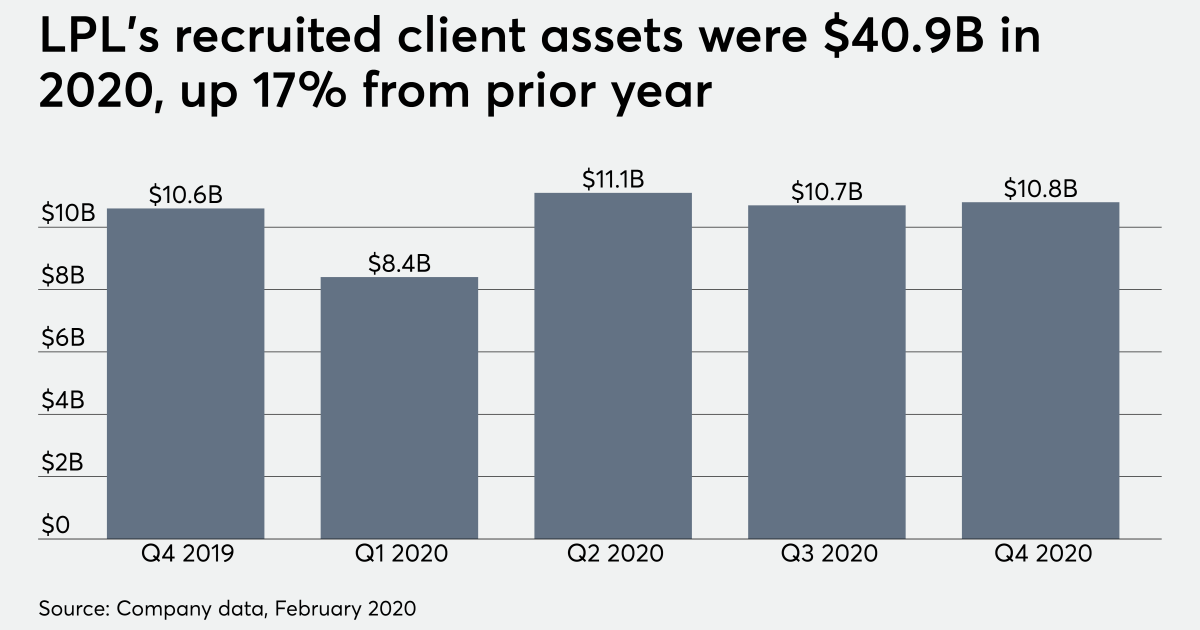

The No. 1 independent broker-dealer’s headcount rose 5% year-over-year — a net 823 advisors — to 17,287 in the fourth quarter, LPL said in reporting its results Feb. 4. LPL also reached new highs in client assets ($903 billion), advisory assets ($461 billion), full-year organic growth ($56.2 billion) and 12-month recruited client assets ($40.9 billion).

Next year will likely bring more expansion, although the new business is bringing higher expenses such as higher compensation on the additional assets and acquisition costs such as LPL’s deal to purchase midsize wealth manager Waddell & Reed for $300 million. The firm aims to keep investing in services like M&A consulting that it could eventually begin offering to non-LPL advisors, CEO Dan Arnold told analysts in an earnings call.

“If we do that well for LPL advisors, then we could easily take that and point that to an advisor that doesn’t necessarily sit on our platform today and help create growth opportunities associated with a practice by providing or plugging in to that type of solution,” Arnold said, according to a transcript by Seeking Alpha.

“It’s logical for us in our overall journey around this play to begin to experiment there and it’s early days of that experiment,” he added. “We will likely take one of these solutions and begin to explore how that might work and present itself outside of the LPL family of advisors.”

The M&A resources rolling out in the first quarter include deal sourcing, advice and capital. LPL has already launched five other subscription outsourced services, which have more than doubled from last year to reach 1,400 users across LPL advisors’ practices, Arnold says.

After a question from an analyst about custodial services, Arnold predicted there will be “more advisor movement or churn across that space” in the next few years and said that LPL seeks “an interesting differentiated solution” for RIAs. The firm has already hired five RIA recruiters who were previously with TD Ameritrade, the website RIABiz reported earlier this week.

Other gains are coming to LPL on the strength of its acquisitions and recruiting in the previous year. The firm picked up $4 billion in client assets in the fourth quarter from two smaller IBDs it bought, E.K. Riley Investments and Lucia Securities, and as many as 900 advisors with $70 billion could move to LPL upon the close of its Waddell & Reed partnership with Australian investment bank Macquarie Group.

LPL expects the incoming advisors to join its ranks in the middle of the year, with the acquiring firm spending an additional $85 million in onboarding expenses such as transition assistance, according to CFO Matt Audette. Waddell & Reed advisors serving approximately 80% of the wealth manager’s assets have committed to LPL, which is above its 70% modeling assumption.

Two massive bank-channel investment programs, M&T Bank and BMO Harris, will generate about $5 million in transition and onboarding expenses as they migrate to LPL from their own broker-dealers in 2021. The firm expects BMO’s advisors to formally affiliate by the end of the first quarter, with M&T’s advisors slated for the middle of the year, Audette notes.

The bank channel represents another area for more potential growth, alongside RIAs and LPL’s new W-2 employee advisor services, Arnold said later in the call. “Certainly this emerging new bank opportunity with respect to larger banks exploring outsourcing is a second way to think about an opportunity going forward,” Arnold said.

For the year, LPL earned net income of $472.6 million on revenue of $5.87 billion — a 16% drop in profit from 2019. The lower figure stemmed from plummeting interest income amid lower rates during the coronavirus, along with higher expenses. Still, its earnings per share prior to intangibles for the fourth quarter of $1.53 was 19 cents above analysts’ consensus.

Following the earnings call, analyst Pauline Bell of independent firm CFRA Research maintained a “strong buy” opinion on LPL’s stock and raised its target price by $25 to $135 per share while lifting its EPS estimate as well.

Expenses remain “well-controlled with higher-than-expected guidance for ’21 more than offset by the continued momentum in organic growth and better-than-forecast Waddell & Reed retention with further upside on greater uptake of business solutions and centrally managed products,” Bell wrote in a note.

Fellow analyst Devin Ryan of JMP Securities rates LPL’s stock as “market perform” after the call, according to his post-earnings note. Ryan “marginally tweaked” LPL’s expected EPS lower for 2021, but he said the firm “reported solid growth” as it leans in on growth investments.

“LPL has performed well against a complicated backdrop in 2020 and enters 2021 with considerable momentum, even as interest rates appear set to remain a headwind,” Ryan said.

Leave a Reply