Forty-five states and Washington D.C. have some type of state sales tax. Some states might even have different sales tax rates or rules for local taxes or online sales. Chances are, your business is probably in a state with sales tax. To remain compliant, you must know sales tax laws by state.

Read on to get the inside scoop about the types of sales tax and what the states with sales tax are.

Sales tax terminology you need to know

Before you dive into this sales tax guide by state, you need to brush up on your sales tax lingo. Below is a brief recap of the different sales tax terms you should know.

Sales tax

Sales tax is a pass-through tax. The tax passes through onto the customer during a transaction. So, who pays sales tax? And, who has to collect sales tax? Customers, not businesses, pay sales tax. However, business owners must collect, deposit, and report the sales tax.

Businesses that need to collect sales tax must do so at the point of sale. Customers purchasing products are responsible for paying the sales tax.

States can also get specific about which products have sales tax. For example, some states charge taxes on groceries while others do not.

Some states have a sales tax holiday during the year. During a sales tax holiday, certain items (e.g., clothing) are exempt from sales tax for a day (or multiple days), week, or weekend.

Sales tax nexus

Sales tax nexus determines whether or not your business has enough presence in a location (e.g., city) to collect sales tax. Certain business activities can determine if you have sales tax nexus in an area.

The following factors generally affect sales tax nexus:

- Your office, warehouse, store, or business location

- Employees, contractors, salespeople, or other personnel

- Amount of sales (e.g., $10,000)

- Trade show sales

Sales tax nexus rules can vary depending on the state. For example, one state may consider a one-day trade show enough of a physical presence to create nexus, while another state may not. Check with your state to find out more details about sales tax nexus rules.

Economic nexus

Economic nexus is when a seller must collect sales tax in a state because they make a certain amount or have a certain number of sales in that state. Economic nexus is similar to sales tax nexus, but for online sales.

Each state with economic nexus laws sets its own threshold that businesses must meet to have economic nexus. Although economic nexus thresholds vary, the most common threshold is when a seller reaches $100,000 in sales or 200 transactions in a year.

More states are jumping aboard the economic nexus train, especially as online sales become more prominent. Be sure to keep an eye out for new economic nexus laws for your state.

Use tax

Use tax is a sales tax that state governments impose on consumers who do not pay sales tax at the time of purchase. You do not collect use tax from customers. Instead, customers pay use tax directly to the applicable state.

Origin-based method

In an origin-based state, sales tax is collected based on the seller’s location. As a business owner, you must collect sales tax based on your state and local tax rates.

Say you operate your business from Ohio. Because the state is origin-based, you need to collect sales tax using Ohio rates.

Destination-based method

In a destination-based state, you must collect sales tax based on the buyer’s location. Collect sales tax based on your customer’s state and local taxes.

Say your business operates in New York and you sell a product to a customer in Brooklyn. Because New York uses the destination-based method, you must collect sales tax based on the customer’s location (Brooklyn).

Determining if you have nexus in a state

If you aren’t sure whether you have sales tax nexus, ask yourself the following questions:

- Do I have a physical presence in the state? (e.g., warehouse, storefront)

- Do I have someone working for me in the state? (e.g., employee, contractor, salesperson)

- Do I have products stored in the state? (e.g., inventory)

- Do my sales numbers or transactions exceed my state’s threshold? (if applicable)

- Do I cross state lines to sell my product? (e.g., trade shows)

If you answered “yes” to any of the above questions, you likely have sales tax nexus. If you’re unsure about whether your business has sales tax nexus, contact your state for additional information.

Breaking down states with sales tax

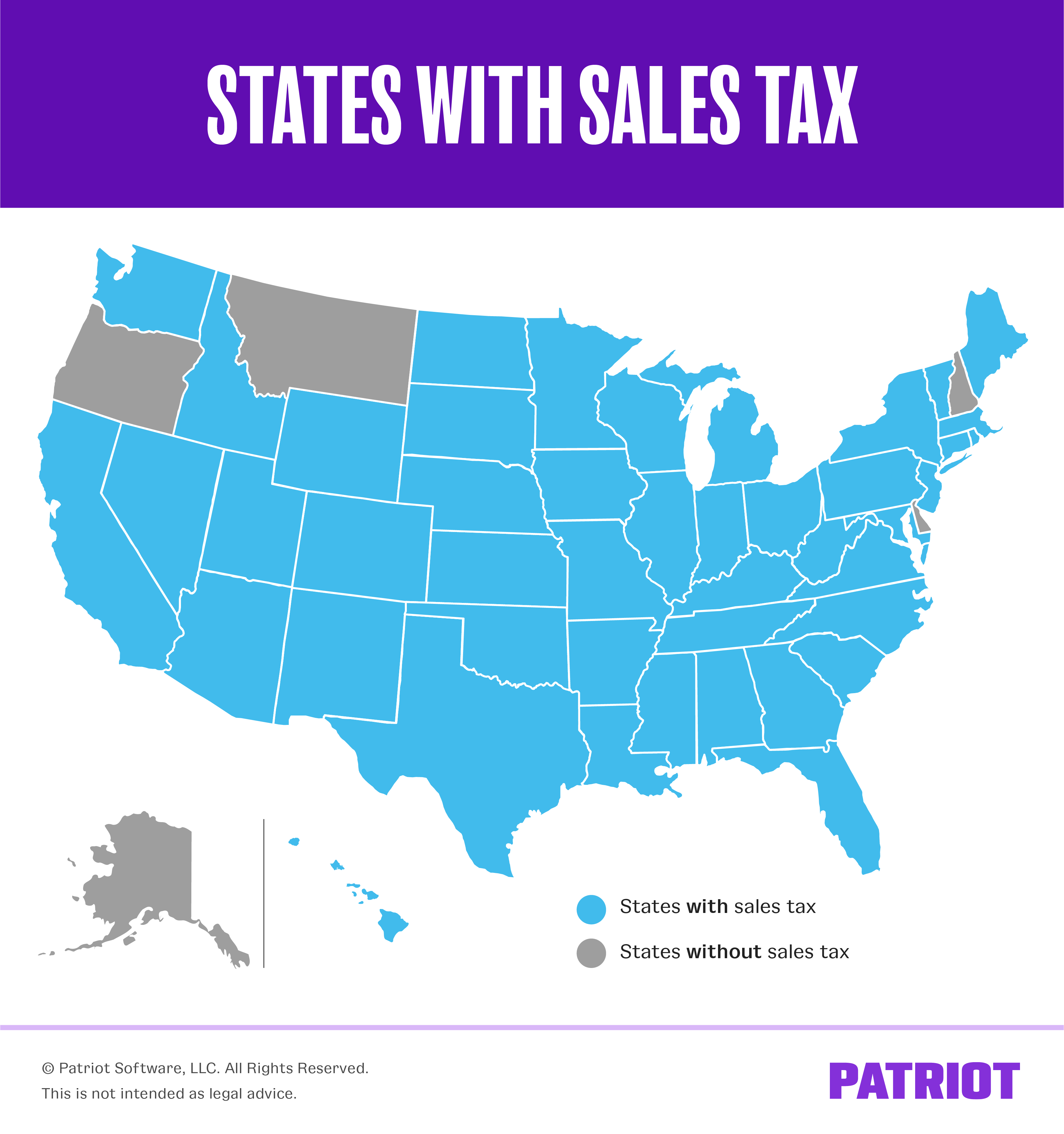

Now that you have a little background on sales tax, let’s take a look at which states have sales tax. Again, 45 states and Washington D.C. have sales tax and different laws in place for sales tax.

Because there are so many states with sales tax laws in place, it may be easier to remember the states with no sales tax. The five states that do not have sales tax are:

- Alaska

- Delaware

- Montana

- New Hampshire

- Oregon

Hawaii also does not have sales tax. However, the state does impose a general excise tax (GET) that’s similar to sales tax on every transaction.

Instead of sales tax, New Mexico has a gross receipts tax (GRT) that you impose on customers in the state.

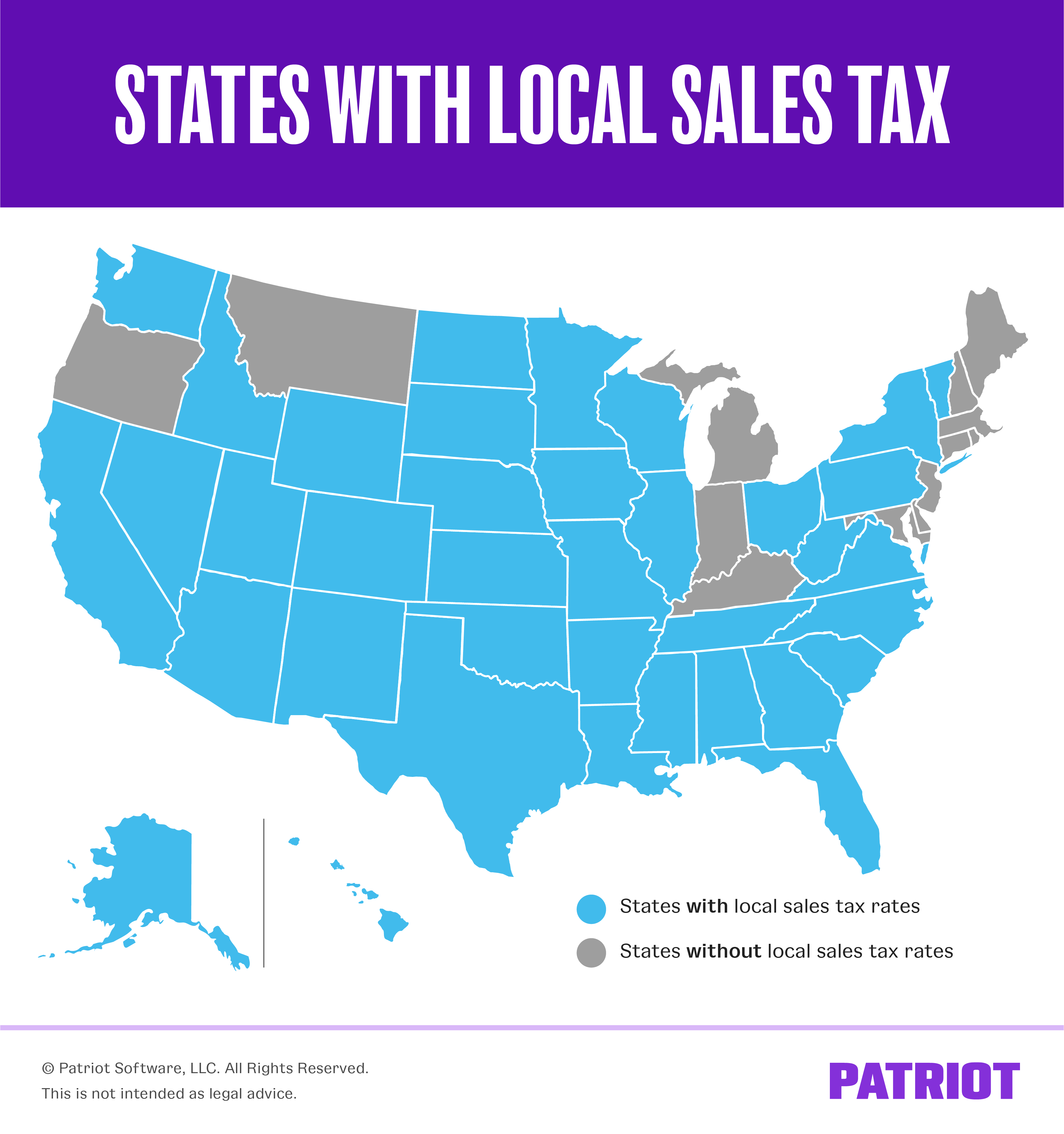

Local sales tax

Many states also require businesses to collect local sales tax, too. The following states don’t have local sales tax:

- Connecticut

- D.C.

- Delaware

- Indiana

- Kentucky

- Maine

- Maryland

- Massachusetts

- Michigan

- Montana

- New Hampshire

- New Jersey

- Oregon

- Rhode Island

Check out the handy map below to find out if your state has local sales tax. Keep in mind that local sales taxes vary from city to city. So, even if you’re located in a state with local sales tax, you might not be responsible for collecting local sales tax.

Sales tax laws by state

Below is a state-by-state breakdown of sales tax laws and rules. Keep in mind that Alaska, Delaware, Montana, New Hampshire, and Oregon do not have sales tax and therefore do not have any sales tax laws. And, remember that sales tax rates vary depending on your business’s location.

Alabama

Alabama has both state and local sales tax. Depending on your location, these laws can vary.

Alabama considers a business to have sales tax nexus if you have one of the following in the state:

- Physical presence in Alabama (e.g., retail store, warehouse, inventory)

- Regular presence of traveling salespeople or agents

- Remote entity nexus (aka economic nexus)

Alabama levies sales tax on the sale of most tangible goods and some services. Some goods are exempt from sales tax under law, such as non-prepared food items, purchases made with food stamps, and prescription drugs.

For more information about sales tax rules in Alabama, check out the state’s website.

Alaska

Alaska does not have state sales tax. Therefore, Alaska does not have any state sales tax laws.

Alaska does have some local areas that might levy sales tax. Check with the state directly to find out whether or not your locality has local tax.

Arizona

Arizona has both local and state sales tax. Sales tax in Arizona is a little different than other states. Some sales taxes might be referred to as transaction privilege tax.

Transaction privilege tax (TPT) is a tax on the privilege of doing business in Arizona. TPT is also collected by businesses and remitted to the state. The business is liable for the tax. However, businesses can pass on the tax to the consumer.

You have sales tax nexus if your business has one of the following in Arizona:

- Employees present in the state conducting business on behalf of the company

- Ownership of property

- Office or place of business in the state

- Delivery of merchandise in vehicles owned by the taxpayer

- Independent contractors or other nonemployee representatives present in Arizona to establish and maintain a market for the taxpayer (e.g., soliciting sales)

Some products are exempt from TPT under Arizona law, including food sold by qualified retailers, prescription drugs, and some medical devices.

Again, the amount of tax you collect can depend on your location. Consult the state for more information about sales tax nexus and rules.

Arkansas

Arkansas has state and local sales taxes. If you own a business in Arkansas, you have sales tax nexus if you have:

- An office or place of business in the state

- A warehouse or agency in Arkansas

- Real or personal property

Arkansas has a destination-based sales tax. No matter if you run your business in Arkansas or outside the state, you charge sales tax at the rate of your buyer’s ship-to location. If you’re outside of Arkansas but have sales tax nexus in Arkansas, you must charge sales tax at the local sales tax rate of the buyer’s ship-to address.

Some customers, like government agencies and nonprofit organizations, are exempt from paying sales tax.

For more information about Arkansas’s sales tax rules, review the state’s website.

California

The California Board of Equalization determines what is considered sales tax nexus in California. Like many other states, California has both local and state sales tax.

According to California law, every retailer engaged in business in the state has sales tax nexus. “Engaged in business” includes:

- Physical location

- A person working for you (e.g., sales rep, agent, contractor, employee)

- An affiliate (e.g., person who refers potential buyers to your business)

- Presence at a trade show

An out-of-state business is “engaged in business” in California if it’s a member of a group in California that helps the out-of-state business establish or maintain a California market for product sales.

Generally, services in California are not taxable. Most tangible products are taxable in California. However, some exceptions include certain groceries, prescription medicine, and medical devices. And, some customers (e.g., nonprofits) do not have to pay sales tax in California if they show a valid certificate.

California is a “hybrid-origin” state when it comes to sales tax collection. This means that they use a mixture of different methods for sales tax collection. With the hybrid method, you collect at least two sales tax rates in California. Collect one for buyers in the area where your business is located and one for buyers outside the area.

For more information about sales tax nexus in California, refer to the California Sales and Use Tax Law.

Colorado

Colorado has state and local sales tax. According to Colorado, a retailer is doing business in the state if it “sells, leases, or delivers tangible personal property or taxable services in Colorado or engages in any activity in Colorado in connection with the selling, leasing, or delivering of tangible personal property or taxable services for use, storage, distribution, or consumption in Colorado.”

You typically have sales tax nexus in Colorado if you have:

- An office, distributing house, sales room, warehouse, or another place of business

- Independent contractors or other representatives in Colorado

Groceries, prescription drugs, and certain medical devices are generally exempt from sales tax in Colorado.

If you’re not based in Colorado but have sales tax nexus, you are considered a remote seller. If you’re a remote seller, you must collect the retailer’s sales tax from Colorado buyers.

Go to Colorado’s website for more information on sales tax rules.

Connecticut

Connecticut has state sales tax but no local sales tax. Connecticut is one of the few states that only has a statewide sales tax. There are no local tax rates, making the tax collection process easier for vendors.

You have sales tax nexus in Connecticut if you have:

- An office or place of business

- An employee, independent contractor, or another representative present in the state for more than two days per year

- Goods in a warehouse

- Ownership of real or personal property

- Economic nexus

Some items, like food products, are exempt from sales tax in Connecticut.

No matter where you’re located (in or out of Connecticut), charge customers in Connecticut a flat 6.35% for sales tax.

For more details, check out Connecticut’s website.

D.C.

You have sales tax nexus in Washington D.C. if you:

- Have an office, place of distribution, sales or sample room, warehouse, storage place, or another place of business

- Have a representative, agent, salesperson, or solicitor to help make retail sales in Washington D.C.

Some items, like non-prepared food items, prescription drugs, machinery, and equipment, are exempt from sales tax in D.C.

Washington D.C. does not charge local sales taxes. This makes it easier for businesses to charge, collect, and remit taxes.

If you have sales tax nexus in Washington D.C., charge the customer 6% sales tax.

Want to learn more about Washington D.C.’s sales tax rules? Take a look at D.C.’s website for more details.

Delaware

Because Delaware does not have any state or local sales tax, the state does not have sales tax laws for business owners.

Florida

Florida has state tax and local tax. You have sales tax nexus if you have any of the following in the state of Florida:

- Ownership of property

- Sales of taxable items (e.g., retail)

- An employee

- Repairs or alterations of tangible personal property

- Rentals, leases, or licenses to use real property

- Rentals of short-term living accommodations

- Rental or lease of personal property

- Manufacturing or producing goods for sale at retail

- Importing goods from any state or country for retail sale

- Providing taxable services (e.g., cleaning services)

Certain groceries, prosthetic or orthopedic instruments, seeds and fertilizers, and cosmetics are considered to be sales tax exempt in Florida.

Florida uses a destination-based sales tax. If you have sales tax nexus in Florida, collect sales tax based off the shipping address.

If you are not based in Florida, you must still charge sales tax based on the buyer’s shipping location.

Review Florida’s website for more information about state-specific sales tax rules.

Georgia

Georgia has both state and local sales tax. Georgia considers sellers to have sales tax nexus if they have one of the following in the state:

- An office or place of business

- An employee, independent contractor, or representative

- Goods in a warehouse

- Ownership of real or personal property

- Delivery of merchandise in Georgia

- Economic nexus

Some items that are sales tax exempt in Georgia include certain types of groceries, medical devices, prescription medications, and machinery or chemicals which are used in development and research.

If you’re in Georgia, collect sales tax based on your buyer’s address. If you operate outside of Georgia, charge sales tax based on the destination of the buyer.

Eager to learn more about Georgia’s sales tax requirements? Check out Georgia’s website for additional information.

Hawaii

Again, Hawaii does not have a general sales tax. However, the state does have a general excise tax law.

Most businesses with any kind of presence in Hawaii, including providing services, are subject to the general excise tax.

The GET rate for Hawaii is 4%. And, local taxes are lower than other states, only getting up to 0.5%.

Idaho

Idaho has both local and state sales tax. If you have one of the following in Idaho, you likely have sales tax nexus:

- Office, warehouse, sales room, or storage place

- Stock of goods

- A property that you rent or lease

- A salesman, agent, employee, or another representative

Some items that may be exempt from Idaho sales tax include prescription drugs, some groceries, truck campers, office trailers, and transport trailers.

If you run your business in Idaho, you must charge sales tax based on your buyer’s location.

If you’re not based in Idaho, you must charge Idaho buyers the 6% sales tax.

Consult the state for more information about Idaho sales tax rules.

Illinois

You generally have sales tax nexus in Illinois if you have one of the following:

- An office, warehouse, or place of business

- An employee, contractor, salesperson, agent, or representative in Illinois

- A third-party affiliate in the state

Some items that are sales tax exempt in Illinois include machinery and building materials for real estate development.

Illinois has origin-based sales tax. If you’re in Illinois, collect sales tax at the rate where your business is located. If you have more than one location, base the rate on your sale’s point of origin.

If you make a sale in Illinois but your business is located outside the state, charge a flat sales tax of 6.25% to Illinois buyers.

For additional details, review Illinois’s website.

Indiana

Indiana has state sales tax but does not have local sales tax. Indiana has a statewide sales tax rate of 7%. You have sales tax nexus in Indiana if you have:

- Tangible property (owned or leased)

- An employee or independent sales representative in the state

- Inventory in the state

- Third parties that install, repair, or service property that is sold to Indiana customers

- Economic nexus

Indiana sales tax does not apply to the sale of food and food ingredients if they are sold unheated and without eating utensils.

For more information about Indiana’s state sales tax rules, consult the state.

Iowa

Iowa has both local and state sales tax. You have sales tax nexus in Iowa if you have or do one of the following:

- An office, warehouse, distribution house, or place of business

- An employee, contractor, or another representative in the state

- Regularly engage in the delivery of products to Iowa

- Economic nexus

Many construction and agriculture items are considered to be sales tax exempt in Iowa. This also includes items for farming and building.

Iowa’s sales tax is destination-based. If your business is located in Iowa, charge sales tax based on the buyer’s location.

If you’re not based in Iowa but have sales tax nexus there, you are considered a remote seller. Remote sellers need to collect the same sales tax as in-state sellers (plus local taxes, if applicable).

For more information about Iowa’s sales tax rules, review the state’s website.

Kansas

Kansas has local and state sales tax. If you have one of the following, you have sales tax nexus in Kansas:

- An office or place of business

- An employee present in Kansas

- Goods in a warehouse

- Retailers selling goods at trade shows, craft shows, or festivals

- Non-resident contractors performing services in the state

In Kansas, construction materials and prescription drugs are typically tax exempt.

Sellers in Kansas should charge sales tax based on the buyer’s location. Out-of-state sellers should also charge sales tax based on the customer’s destination.

For additional information about Kansas’s sales tax regulations, take a look at Kansas’s website.

Kentucky

Kentucky considers a seller to have sales tax nexus if they have any of the following:

- Owned or leased property that is utilized or located in the state

- An employee or contractor

- Goods in a warehouse

- Services completed in the state

- Computer software used by a third party in the state

- Craft, trade show, or festival participation for 15 or more days per year

- Economic nexus

In Kentucky, farming equipment, prescription medication, and equipment used for construction are sales tax exempt.

Kentucky does not have local tax rates. If your business has sales tax nexus in Kentucky, you must charge a 6% sales tax to Kentucky buyers. Out-of-state businesses with sales tax nexus in Kentucky must also charge 6%.

Craving more information? Check out Kentucky’s website for more details on sales tax rules.

Louisiana

Louisiana’s general sales tax is levied on the following types of transactions:

- Sale of tangible personal property

- The use, consumption, distribution, or storage of tangible property

- The lease or rental of any item of tangible property

- Sale of services

Generally, food for home consumption, prescription medicine, and utilities are tax exempt in Louisiana.

The Louisiana state sales tax rate is currently 4.45%. Depending on your locality, the total tax rate can be as high as 11.45%.

For additional information, check out Louisiana’s website.

Maine

Maine has state sales tax but does not have local sales tax. You typically have sales tax nexus in the state of Maine if you have:

- A store, office, warehouse, repair facility, or another place of business in the state

- An employee, salesperson, contractor, or another representative

- Economic nexus

Grocery products, certain types of prescription medication, and some medical equipment are sales tax exempt in Maine.

The state sales tax rate in Maine is 5.5%. Maine does not have local sales tax rates. Therefore, you would charge your customer 5.5%, regardless of whether your business is based and operates in Maine.

Need more information? Review the state’s website for additional sales tax details.

Maryland

Like Maine, Maryland has state sales tax, but does not have local sales tax. In Maryland, you have sales tax nexus if you have one of the following in the state:

- An office or place of business

- An employee present in the state

- Goods in a warehouse

- Ownership of real (e.g., land) or personal property

Some purchases and products are tax exempt in Maryland, including non-prepared foods, farm equipment, and certain machinery.

How you collect sales tax for Maryland depends on whether you’re in- or out-of-state. If your business is in Maryland, collect sales tax based on where your customer lives. Sellers who make a sale in Maryland but work outside of the state must charge sales tax based on the destination of the buyer. Regardless of if you’re in- or out-of-state, you must collect 6% sales tax from Maryland customers.

To learn more about Maryland’s state sales tax rules, check out the state’s website.

Massachusetts

Massachusetts only has state sales tax. A business or vendor has sales tax nexus in the state of Massachusetts if they have or do one of the following:

- An office, place of business, or any owned property

- An employee present for more than two days per year

- Goods in a warehouse

- Ownership of real or personal property

- A sample or display area (e.g., trade show exhibit)

- Deliver property or performance of service

- Economic nexus

Some products exempt from sales tax in Massachusetts include food for human consumption (other than meals sold by a restaurant), sales of utilities and heating fuel, newspapers, and magazines.

Massachusetts only has a statewide sales tax of 6.25%. Use this same percentage regardless of whether you or your business is located in Massachusetts. Charge 6.25% of sales tax to buyers in Massachusetts.

Learn more about Massachusetts’s sales tax rules by visiting the state’s website.

Michigan

Michigan has state sales tax and does not have local sales tax.

Under state law, Michigan considers you to have sales tax nexus if you sell tangible personal property to a consumer. You have nexus with Michigan if you:

- Are physically present in the state for more than one day OR

- Actively solicit sales in Michigan and have gross receipts of $350,000 or more OR

- Have ownership or beneficial interest in a flow-through entity which has substantial nexus in the state

Because there are no local tax rates in Michigan, you only need to worry about the statewide sales tax rate of 6%. Both Michigan-based and remote sellers (e.g., out-of-state) must use the 6% rate when charging customers sales tax.

For more information, check out Michigan’s Department of Treasury website.

Minnesota

Minnesota has both state and local sales tax. The state of Minnesota considers you to have sales tax nexus if you:

- Have an office, distribution center, sales room, warehouse, or another place of business in the state

- Have a representative, agent, salesperson, or solicitor (both permanent and temporary)

- Deliver items into Minnesota in your own vehicle

- Provide taxable services

- Have an agreement with a solicitor for the referral of Minnesota customers for a commission and your gross receipts are at least $10,000 over the course of 12 months

Certain grocery items and prescription and over-the-counter drugs are tax exempt in Minnesota.

Minnesota has destination-based sales tax. Collect sales tax at the rate of your customer’s ship-to address.

For additional information about Minnesota’s sales tax rules, check out the state’s website.

Mississippi

There are both state and local sales taxes in Mississippi. In Mississippi, state law says you have sales tax nexus in the state if you:

- Own business property in the state

- Have employees or agents of the business provide services in Mississippi

Some goods exempt from Mississippi sales tax include non-prepared food items, medical supplies, and some prescription drugs.

The sales tax you collect depends on whether you’re based in Mississippi or out-of-state. Mississippi has origin-based sales tax. If you’re in Mississippi, collect sales tax at the tax rate where your business is located.

If you have more than one location in Mississippi, charge sales tax based on your sale’s point of origin.

If you are out-of-state but have sales tax nexus for Mississippi, you are only required to charge a 7% sales tax.

Want to learn more about Mississippi’s state sales tax law? Take a look at Mississippi’s FAQs for additional information.

Missouri

Like many other states, Missouri has both state and local sales tax. You have sales tax nexus in Missouri if you:

- Have an office or place of business

- Have an employee, contractor, or another representative present in the state for more than two days per year

- Have goods in a warehouse

- Own real or personal property

- Deliver merchandise in Missouri in vehicles you own

Some medical devices, certain prescription medication, and agricultural machinery and chemicals are generally sales tax exempt in Missouri.

Missouri is origin-based. If you’re in Missouri, you must collect sales tax at the tax rate where your business is located.

If you are not based in Missouri, the state considers you a remote seller. As a remote seller, you must collect sales tax, which is at a rate of 4.225%.

For more information about sales tax in Missouri, check out the state’s website.

Montana

Montana does not have any sales tax (including local sales tax). So, the state does not have any sales tax laws.

Although Montana does not have any local taxes, some areas in the state may levy a sales tax on tourism-related transactions. Check with Montana for more information about tourism-related sales tax.

Nebraska

Nebraska has both state and local sales tax. You have sales tax nexus in Nebraska if you have any of the following in the state:

- An office or place of business

- Employee, agent, salesperson, or contractor present in the state

- Ownership of or goods in a warehouse or storage facility

- Receipts from rental or lease of property

Certain types of prescription medications and medical devices may be exempt from Nebraska sales tax.

Nebraska uses the destination-based sales tax method. No matter if you run your business in or outside of Nebraska, charge sales tax based on the buyer’s ship-to location.

Check out more information about Nebraska’s sales tax laws by reviewing the state’s website.

Nevada

Nevada has state and local sales tax. Nevada considers a business to have sales tax nexus if you have any of the following in the state:

- An office or place of business

- An employee, independent contractor, or representative in the state

- Goods in a warehouse

- Ownership or real or personal property

- Delivery of merchandise in Nevada using company vehicles

Items that are not taxable include unprepared food; farm machinery and equipment; newspapers; and interest, finance and carrying charges on credit sales.

If you’re in Nevada, you must collect sales tax based on where your customer lives. If your business is based outside of Nevada, charge sales tax based on the buyer’s destination.

For additional information, check out Nevada’s Department of Taxation FAQs.

New Hampshire

New Hampshire does not have state or local sales tax or any sales tax laws. The state also does not have any local sales tax.

New Jersey

New Jersey has state sales tax. However, it does not have local sales tax. In New Jersey, you have sales tax nexus if you have or do one of the following in the state:

- An office or place of business

- An employee, independent contractor, or representative in the state

- Goods in a warehouse

- Ownership or real or personal property

- Delivery of merchandise in New Jersey

- Provide any maintenance program

Grocery items, prescription drugs, and over-the-counter drugs are generally sales tax exempt.

Again, New Jersey does not have any local sales tax rates. If you have sales tax nexus in New Jersey, charge customers 6.625% for sales tax.

Want more information? Check out New Jersey’s Sales Tax Guide.

New Mexico

New Mexico’s sales tax may also be referred to as gross receipts tax, or GRT. Businesses in New Mexico impose GRT on customers instead of sales tax.

New Mexico’s GRT is sometimes already included as a part of the selling price.

In most cases, sales and leases of goods and property (tangible and intangible) are taxable. Unlike many other states, sales and performances are taxable in New Mexico.

For sellers in New Mexico, GRT is based on the business location of the seller.

If your business location is outside of New Mexico, you must only collect a flat GRT tax of 5.125%.

To learn more about New Mexico’s gross receipts tax, check out New Mexico’s Taxation & Revenue website.

New York

There are state and local sales taxes in New York. You have sales tax nexus in New York if you have one of the following in the state:

- An office or place of business

- An employee, independent contractor, or representative in the state

- Goods in a warehouse

- Ownership or real or personal property

- Delivery of merchandise in New York in a taxpayer-owned vehicle

Services are generally exempt from New York sales tax unless they are specifically taxable. Check out a full list of exemptions here.

New York is a destination-based sales tax state. If your business is located in New York, charge customers sales tax based on where you’re delivering the item to. Depending on the delivery location, the sales tax rate might include a combination of state, county, city, and district tax rates.

If your business is located outside of New York state, charge sales tax based on the buyer’s destination.

For more information about New York’s sales tax rules, check out the state’s website.

North Carolina

North Carolina has both state and local sales tax. A seller has sales tax nexus in North Carolina if they have any of the following in the state:

- An office or place of business

- Employees, independent contractors, agents, or other representatives

- Any place of distribution; sales or sample room; warehouse; or storage place that you manage, use, or occupy temporarily or permanently

Some items exempt from North Carolina’s sales tax include prescription medications, some groceries, and machinery.

North Carolina has destination-based sales tax. If you’re in North Carolina, your buyer’s location dictates how much you collect for sales tax.

Regardless of if you’re based in North Carolina or not, you must charge sales tax based on the customer’s ship-to location if you have sales tax nexus.

To learn more about North Carolina’s sales tax rules, check out NC’s Department of Revenue website.

North Dakota

Like many other states, North Dakota has both state and local sales tax. You have sales tax nexus in North Dakota if you have one of the following in the state:

- A temporary or permanent office or place of business

- An employee or agent in the state

- Tangible personal property (leased or rented)

- Economic nexus

Some computer and telecommunications equipment and machinery and chemicals for agriculture are exempt from sales tax in North Dakota.

Because North Dakota is a destination-based sales tax state, it does not matter if your business is inside or outside of North Dakota. Regardless of where you’re located, you must collect sales tax from your customers based on their ship-to location.

Check out North Dakota’s website for additional information about sales tax laws.

Ohio

Ohio has state sales tax. And, some areas have local sales tax laws. In Ohio, you have sales tax nexus if you:

- Have a place of business that’s operated by employees or agents, a member of an affiliated group, or a franchisee

- Have employees, agents, representatives, solicitors, installers, repair people, salespeople, or other individuals in Ohio

- Have a person in the state for the purpose of receiving or processing orders

- Make regular deliveries of tangible personal property into the state

- Own tangible personal property that is rented or leased to a consumer in this state

- Offer tangible personal property, on approval, to consumers in this state

- Own, rent, lease, maintain, or use tangible personal or real property that is located in Ohio

- Are registered with the secretary of state to do business

- Are licensed by any state agency, board, or commission to do business in Ohio or to make sales to Ohio customers

- Make more than $500,000 in sales in the state and use software or content delivery network

In Ohio, many food items and groceries are exempt from sales tax. However, this does not generally include meals sold by restaurants.

Ohio uses the origin-based sales tax method. If your business is located in Ohio, collect sales tax depending on where your business is located. If you have more than one location in Ohio, base the sales tax on the sale’s point of origin.

If your business is located outside of Ohio, charge sales tax based on the buyer’s destination.

Want more information? Take a look at Ohio’s Department of Taxation website.

Oklahoma

Oklahoma has local and state sales tax. You have sales tax nexus in Oklahoma if you:

- Have an office or place of business in the state

- Have a salesperson, contractor, installer, or other representative doing business in the state

- Have goods in a warehouse, distribution center, or another place of business

- Deliver merchandise in Oklahoma in taxpayer-owned vehicles

Purchases made with food stamps, prescription drugs, and some manufacturing equipment are sales tax exempt in Oklahoma. For a full list of exemptions, check out this list.

If you’re an Oklahoma-based business selling to an Oklahoma customer, charge sales tax based on the customer’s ship-to address.

If you have sales tax nexus but do not operate in Oklahoma, you must still collect sales tax from customers.

For more information about Oklahoma sales tax regulations, take a look at the Oklahoma Tax Commission’s website.

Oregon

Oregon does not have state or local sales tax. Therefore, it does not have any sales tax laws to follow.

Pennsylvania

Pennsylvania has state and local sales tax. Pennsylvania considers businesses to have sales tax nexus if they have or do one of the following in the state:

- An office or place of business

- An employee, independent contractor, or another representative

- Goods in a warehouse

- Ownership of real or personal property

- Lease property in the state

- Deliver merchandise in Pennsylvania

Some items exempt from sales tax in Pennsylvania include food (not ready-to-eat), candy, gum, most clothing, textbooks, computer services, and pharmaceutical drugs.

Pennsylvania is an origin-based sales tax state. If your business is in Pennsylvania, collect sales tax based on your business’s location. Charge sales tax based on the sale’s point of origin if you have more than one location in the state.

If you have nexus in Pennsylvania but are located outside of the state, charge customers the 6% tax rate.

Currently, there are only two locations in Pennsylvania that have a local tax rate: Allegheny County and Philadelphia. Every other location only uses the statewide 6% sales tax rate.

Check out Pennsylvania’s Department of Revenue website for more information.

Rhode Island

Rhode Island has state sales tax, but no local sales tax. You have sales tax nexus in the state of Rhode Island if you have one of the following:

- An office or place of business

- An employee, representative, contractor, agent, or salesperson present in the state

- Goods in a warehouse, sample room, or storage room

- Delivery of merchandise to customers in the state using the business’s owned vehicle

- Advertising in the state

- A third-party affiliate

- Attendance at a tradeshow or craft show

Examples of items that are exempt from sales tax in Rhode Island include some food and certain medical items.

Rhode Island is a destination-based sales tax state. Charge customers in Rhode Island sales tax based on their ship-to location regardless of whether or not your business is located in Rhode Island.

Rhode Island does not have any local sales taxes or laws. Because of this, you must only charge the statewide 7% sales tax to each buyer in Rhode Island.

For additional information, check out Rhode Island’s website.

South Carolina

South Carolina has both state and local sales tax. You have sales tax nexus in South Carolina if you:

- Have an office or place of business

- Have an employee, independent contractor, or representative

- Have goods in a warehouse

- Own real or personal property

- Deliver merchandise in South Carolina in taxpayer-owned vehicles

Non-prepared foods are sales tax exempt in South Carolina.

Because South Carolina uses the destination-based sales tax method, you must collect sales tax based on your customer’s location.

Check out the state’s website for more information on sales tax rules.

South Dakota

There is both state and local sales tax in South Dakota. Generally, you have sales tax nexus in South Dakota if you have:

- A physical presence in the state (e.g., retail store, warehouse, inventory)

- Regular presence of traveling salespeople or representatives

Economic nexus

Certain items, like farm machinery and prescription medications are exempt from sales tax in South Dakota.

For more details on South Dakota’s sales tax rules, take a look at the state’s website.

Tennessee

Tennessee has both state and local sales tax. You have sales tax nexus in the state of Tennessee if you have one of the following:

- A corporate presence

- An employee, independent contractor, or representative in the state

- Tangible personal property (leased or rented)

- Ownership of real or personal property

- Economic nexus

Certain food items, medical supplies, agricultural equipment, and machinery are exempt from sales tax in Tennessee.

If you’re in Tennessee, collect sales tax based on where your business is located.

To learn more about Tennessee’s sales tax rules, check out the state’s tax guide.

Texas

Texas has state and local sales tax. In Texas, you have sales tax nexus if you have:

- An office or place of business

- An employee

- A place of distribution, sales room, warehouse, or storage space

Some grocery and convenience store items are exempt from sales tax in Texas.

If you live in Texas, you must collect sales tax depending on where your business is located.

If your business is located outside of Texas, charge sales tax based on the customer’s shipping address.

For more information, check Texas’s Comptroller website.

Utah

There are local and state sales taxes in Utah. You may have nexus in Utah if you have:

- A physical presence in the state (e.g., employees or property)

- Ownership in a business with a presence in Utah

- Economic nexus

Certain equipment and machinery, prescriptions drugs, and food are sales tax exempt in Utah. Check out the state’s full list here.

For more information about Utah’s sales tax rules, review the state’s website.

Vermont

Vermont has state and local sales tax. According to Vermont, you must charge a state sales tax of 6% on the retail sales of tangible personal property. You generally have sales tax nexus with Vermont if you have:

- Physical presence in the state (e.g., retail store, warehouse, inventory, etc.)

- Regular presence of traveling salespeople or representatives

Certain clothing, over-the-counter drugs, food and beverages, and medical equipment and supplies are exempt from sales tax in Vermont.

Check out more information about Vermont’s sales tax rules by visiting the state’s website.

Virginia

There are both state and local sales taxes in Virginia. Your business has sales tax nexus in Virginia if you have any of the following in the state:

- An office or place of business

- An employee or independent contractor in the state

- Goods in a warehouse

- Ownership of real or personal property

- Leased property

- More than 12 deliveries or merchandise per year

- Advertisements in newspapers, periodicals, billboards, or posters (not delivered by mail)

Certain items, like agricultural materials and equipment, newspapers and magazines, prescription drugs, and medical equipment are exempt from sales tax in Virginia. Take a look at Virginia’s website for a full list of tax-exempt items.

If your business is located in Virginia, collect sales tax at the rate where your business is located (origin-based sales tax).

If you make a sale to someone in Virginia and your business is out-of-state, charge sales tax according to the buyer’s destination.

To find out more about Virginia’s sales tax laws, check out the state’s website.

Washington

Washington state has both state and local sales tax. A business has sales tax nexus in Washington if you:

- Solicit sales in Washington through employees or representatives

- Install or assemble goods in the state

- Maintain a stock of goods (e.g., inventory)

- Rent or lease tangible personal property

- Provide services in the state

- Construct, install, repair, or maintain real or personal property

- Make regular deliveries of goods into the state

Most non-prepared food items, prescription drugs, and some machinery and equipment are sales tax exempt in Washington.

For additional information about sales tax laws in Washington, take a look at the state’s website.

West Virginia

There are both state and local sales taxes in West Virginia. West Virginia law states all sales of goods and services are subject to sales and use tax unless an exemption is clearly stated. You must impose sales tax on the sale of goods and services at the time of purchase.

A business typically has nexus in West Virginia if it has:

- Physical presence in the state (e.g., retail store, warehouse, inventory, etc.)

- Regular presence of traveling salespeople or representatives

Some machinery and equipment and medical equipment and paraphernalia are exempt from West Virginia sales tax. Check out a detailed list of what is exempt here.

Review West Virginia’s Tax Department website for additional details on sales tax requirements.

Wisconsin

Wisconsin has state and local sales taxes. Your business has sales tax nexus in Wisconsin if you have one of the following:

- An office or place of business

- An employee present in the state

- Goods in a warehouse

- Ownership of real or personal property

- Economic nexus

Certain grocery items, prescription medicine and medical devices, and certain pieces of manufacturing equipment are sales tax exempt in Wisconsin.

If your business is in Wisconsin, collect sales tax based on where you’re delivering the item to. If your business is not in Wisconsin, you must still collect sales tax based on the customer’s ship-to location.

For more information about Wisconsin’s sales tax requirements, check the state’s website.

Wyoming

Wyoming has local and state sales tax. You typically have sales tax nexus in the state of Wyoming if you:

- Have an office, warehouse, plant, or other business location

- Have employees or contractors in the state

- Conduct marketing activities in the state (e.g., advertising)

Some items are exempt from sales tax in Wyoming, including agricultural products, construction services, mining products, and manufacturing equipment.

Learn more details about Wyoming’s sales tax rules by visiting the state’s website.

Sales tax by state: 2021 rates and sales tax method

Now that you know the ins and outs of each state’s sales tax laws, let’s briefly go over sales tax basics for each state. Below is a handy chart to determine your local and state sales tax rates and whether your state uses origin vs. destination sales tax.

| State | 2021 Sales Tax Rate | 2021 Local Tax Rates | Sales Tax Method |

|---|---|---|---|

| Alabama | 4% | 0% – 7% | Destination-based |

| Alaska | N/A | 0% – 7.5% | N/A |

| Arizona | 5.6% | 0% – 5.3% | Origin-based |

| Arkansas | 6.5% | 0% – 5.5% | Destination-based |

| California | 7.25% | 0% – 3.5% | Hybrid of both (State, county, and city taxes are origin-based, but district transaction taxes are destination-based) |

| Colorado | 2.9% | 0% – 8.3% | Destination-based |

| Connecticut | 6.35% | N/A | Destination-based |

| Delaware | N/A | N/A | N/A |

| D.C. | 6% | N/A | Destination-based |

| Florida | 6% | 0% – 2.5% | Destination-based |

| Georgia | 4% | 0% – 5% | Destination-based |

| Hawaii | 4% | 0% – 0.5% | Destination-based |

| Idaho | 6% | 0% – 3% | Destination-based |

| Illinois | 6.25% | 0% -4.75% | Origin-based |

| Indiana | 7% | N/A | Destination-based |

| Iowa | 6% | 0% – 1% | Destination-based |

| Kansas | 6.5% | 0% – 4.1% | Destination-based |

| Kentucky | 6% | N/A | Destination-based |

| Louisiana | 4.45% | 0% – 7% | Destination-based |

| Maine | 5.5% | N/A | Destination-based |

| Maryland | 6% | N/A | Destination-based |

| Massachusetts | 6.25% | N/A | Destination-based |

| Michigan | 6% | N/A | Destination-based |

| Minnesota | 6.875% | 0% – 2% | Destination-based |

| Mississippi | 7% | 0% – 1% | Origin-based |

| Missouri | 4.225% | 0% – 5.875% | Origin-based |

| Montana | N/A | N/A | N/A |

| Nebraska | 5.5% | 0% – 2% | Destination-based |

| Nevada | 6.85% | 0% – 3.665% | Destination-based |

| New Hampshire | N/A | N/A | N/A |

| New Jersey | 6.625% | N/A | Destination-based |

| New Mexico | 5.125% | 0% – 3.9375% | Origin-based |

| New York | 4% | 0% – 4.875% | Destination-based |

| North Carolina | 4.75% | 0% – 2.75% | Destination-based |

| North Dakota | 5% | 0% – 3.5% | Destination-based |

| Ohio | 5.75% | 0% – 2.25% | Origin-based |

| Oklahoma | 4.5% | 0% – 6.5% | Destination-based |

| Oregon | N/A | N/A | N/A |

| Pennsylvania | 6% | 0% – 2% | Origin-based |

| Rhode Island | 7% | N/A | Destination-based |

| South Carolina | 6% | 0% – 3% | Destination-based |

| South Dakota | 4.5% | 0% – 2% | Destination-based |

| Tennessee | 7% | 0% – 2.75% | Origin-based |

| Texas | 6.25% | 0% – 2% | Origin-based |

| Utah | 4.85% for the state sales tax rate. The combined rate with local sales tax can be higher. | 0% – 4.2% | Origin-based |

| Vermont | 6% | 0% – 1% | Destination-based |

| Virginia | 5.3% | 0% – 1.7% | Origin-based |

| Washington | 6.5% | 0% – 4% | Destination-based |

| West Virginia | 6% | 0% – 1% | Destination-based |

| Wisconsin | 5% | 0% – 0.6% | Destination-based |

| Wyoming | 4% | 0% – 2% | Destination-based |

Remember that sales tax rates (both statewide and local rates) are ever changing. Be sure to check your rates at the beginning of each year to ensure they have not changed.

In addition to rates changing, sales tax laws are always evolving, too. Keep up with your sales tax laws annually to make sure you’re compliant with your state’s sales tax rules.

| Does your business have sales out-of-state? If so, you might have economic nexus in another state. Check out our Guide to Economic Nexus Laws by State article to learn whether or not you have economic nexus in a certain state. |

Looking for an easy way to track your state’s sales tax and business transactions? Patriot’s online accounting software lets you streamline the way you record your business’s income and expenses. Get started with a free trial today!

This article has been updated from its original publication date of July 30, 2019.

This is not intended as legal advice; for more information, please click here.

Leave a Reply