Executive Summary

Ten years ago, when robo-advisors exploded onto the scene, their prediction was that they could do what financial advisors do at a fraction of the cost, and put the humans out of business. A decade later, though, the reality is that human financial advisors are still surviving and even thriving, increasingly leveraging “robo” tools and business process automation to make our own advisory firms more efficient. In fact, the irony is that the ongoing rise of technology in financial advisory firms isn’t putting financial advisors out of jobs; instead, it’s replacing back-office jobs with technology and actually elevating the role of the financial advisor within the firm in providing that proverbial “last mile” of service, support, and most importantly advice, to the end client.

At the same time, though, technology itself is taking on an increasingly central role in the advisory firm, making the business more reliant than ever on finding the best and right technology solution to help the firm achieve its own business goals. Which is no small feat, given what are now more than 300 independent advisor technology solutions tracked by Kitces Research across the AdvisorTech landscape, deployed across a wide range of industry channels (from RIAs to broker-dealers, insurance companies to bank and trust companies) and business models (from commissions to AUM fees to monthly subscriptions and other fee-for-service models).

Over the years, industry surveys have attempted to get a handle on trends in advisor technology adoption, exploring the most popular and well-rated solutions. Except most advisor technology surveys in the industry are either too small to form a sufficient sample, unwittingly biased towards some industry channels over others, or implemented via open survey links that anyone can take (which in turn are distributed by the technology vendors themselves and distort the results by whichever companies do the best job at turning out their own power users to participate).

In this context, we’re excited to announce the launch of the latest Kitces Research study, on Advisor Technology. Leveraging our own core strengths – a team of nerdy PhDs trained in research methods and survey methodology – this latest Kitces Research study will be unique in that there will be no open survey links distributed via this blog, social media, or industry technology vendors. Instead, participation in this latest Kitces Research study will be “by invitation only”, through a combination of emails, telephone calls, and even snail mail (yes, really!), in an attempt to gather together the most representative sampling of the true trends in advisor technology across the advisor ecosystem.

Ultimately, our goal is simply to answer the questions most relevant to financial advisors – from solo firms to large-scale enterprises – trying to make their own technology decisions, who want to understand what other firms are really using (or not), and what is actually well-rated amongst advisors (or not) – as well as to glean the trends of what’s becoming more and less popular, where should firms consider developing their own solutions instead of going with what’s available in the marketplace, where might venture capital and private equity firms deploy their own dollars to pursue the biggest opportunities for impact in the advisor marketplace, and what parts of the advisor technology stack are most ripe for innovation and prone to disruption.

In the meantime… please stay tuned for your potential invitation to participate in the Kitces Research study on Advisor Technology!

The Ongoing Evolution Of The AdvisorTech Landscape

When personal computers first showed up in the offices of financial advisors in the 1980s, it was not only expensive to buy a computer, it was also incredibly expensive to make software for those computers and their users. Software went through extensive (and expensive) phases of building and testing because once it was ready, it had to be mailed – via physical disks – for the end-user to install and begin to use. Which meant the software had to be “right” from the start (because the next version might not be released for another year or more!) and required a substantial base of users to amortize the cost of development and generate a profit in the first place.

In fact, the development of software was so expensive and cumbersome that in practice, it was only economically feasible to do so if the software would be sold to large-scale advisor enterprises, and/or was outright developed by those enterprises for their own base of advisors. Which gave those advisor enterprises proprietary software capabilities that helped them compete for advisor talent in the marketplace. And effectively built “moats” around their advisors that prevented them from leaving, because those software solutions only worked for the advisors of the firm, in a world where internally developed proprietary software didn’t (and realistically, couldn’t) integrate with anything else.

By the late 1990s, these trends culminated in the largest advisory firms with the largest base of advisor users (e.g., large wirehouses and major insurance companies) having the best and most capable and most deeply integrated software, while smaller and more independent advisory firms languished, making do with their own homegrown solutions built on top of ‘basic’ office applications like Word and Excel.

And then the internet showed up, and everything changed.

The first major breakthrough of the internet was that it changed how software was developed and distributed. Suddenly, it was no longer necessary to build the entire solution upfront, at once, before it was mailed out to users as “the software” until the next major version release; instead, users could download patches, or entirely new versions of the software, as they became available. Which shortened development cycles, increased the pace of iterative improvements, and also made it easier to sell the software and get it into the hands of new users (who could simply “buy online”, download the software, and begin using it immediately).

The second major breakthrough of the internet was the rise of Application Programming Interfaces (APIs), which for the first time made it possible for independently developed software solutions to open up pathways for other independently developed software solutions to connect and pass data between each other. And suddenly, it became possible for independent advisor software solutions to integrate with one another, without necessarily requiring a centralized enterprise to design, build, and control the integration process. In the two decades since, there has been a veritable explosion of independent advisor software solutions, all using APIs to interface with each other in a rich ecosystem that couldn’t have been imagined just a decade or two prior.

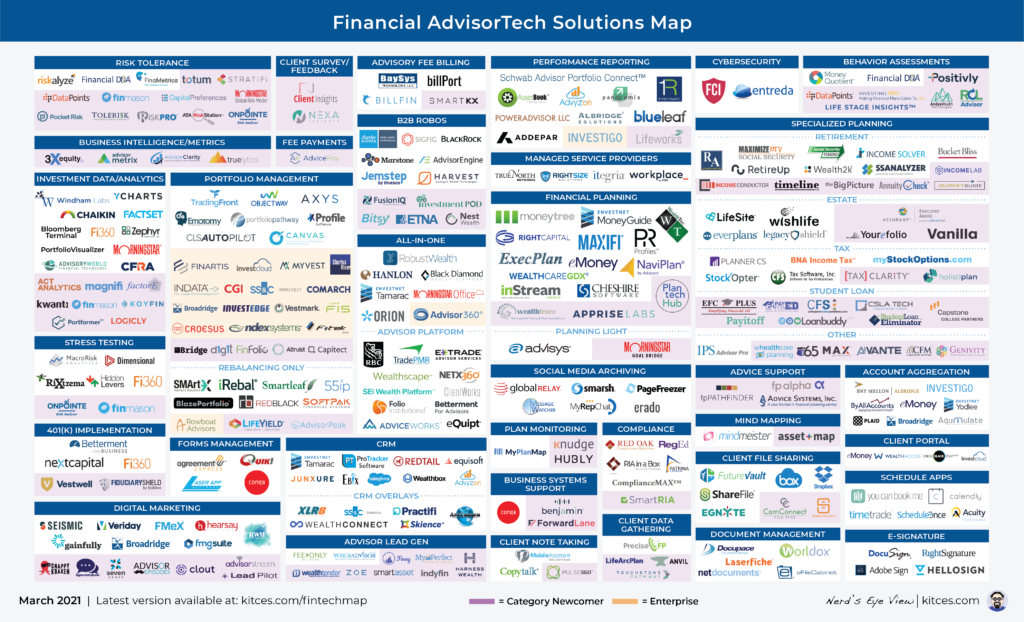

Click Map For A Larger Version

The end result of this shift is that our Financial AdvisorTech Solutions Map now tracks more than 300 different software solutions for independent advisors, and the largest independent vendors have 10s of thousands of advisor users, far more than even the largest advisor enterprises (e.g., wirehouses or independent broker-dealers like LPL) that cap out at “just” 15,000–20,000 advisors each.

Advisor Industry Fragmentation And The Balkanization Of Advisor Software

Despite the tremendous growth of the financial advice business over the past several decades, the sad irony is that “financial advice” itself is not actually regulated as such; instead, financial advisors are regulated by how they are paid or what is implemented at the end of the advice process, with those implementing insurance products overseen by state insurance regulators, those who sell investment products overseen by FINRA, and those who provide ongoing investment management regulated by either the SEC or their state securities regulator (which in turn depends on how many clients they have and the total amount of client assets that they manage).

The significance of these regulatory delineations is that it results in a massive fragmentation of the financial advisory industry across different channels (insurance products, securities products, and investment management, not to mention banking and trust companies living in their own world with their own regulators), which in turn is further compounded by the split between “employee” advisor models (e.g., captive insurance companies, wirehouses, and enterprise RIAs) and “independent” advisor models (e.g., independent annuity agents operating through IMOs, independent broker-dealers, and independent RIAs). And the differences in those advisor industry channels and firm types lead to varying demands for features based on their core business model, varying capabilities to deploy and implement technology based on their size, and varying needs for integrations to the other solutions they also use (based, again, on those channel and size distinctions).

In other words, the software needed by a solo advisor at an independent RIA charging financial planning fees differs completely from what’s needed by a wirehouse with 15,000 employee advisors selling investment products, which is entirely different from what an independent broker-dealer would need for its 5,000 non-employee registered representatives selling investment products in their own local practices, which shares little in common with the needs of an enterprise RIA with 200 employee advisors providing comprehensive financial planning services alongside the company’s centralized portfolio management offering.

In fact, the sea of advisor fragmentation – with nearly 200,000 financial advisors spanning across more than 3,500 broker-dealers, tens of thousands more advisors at the nearly 13,000 SEC-registered RIAs (and potentially even more state-registered RIAs), hundreds of thousands of insurance agents, and substantial overlap across those various categories due to multi-licensed “dual-registrants” – the reality is that it’s incredibly difficult for advisor software companies to distribute their software to the advisor community, particularly in recent decades where the growing trend of independence means more opportunity to sell to advisors directly without enterprise gatekeepers (which can speed innovation and the ability to quickly capture market share), but the fragmentation makes it brutally difficult to find and reach those advisors any faster than one at a time (which is not economical when growing and scaling a software company).

For most software providers, the fragmentation of the advisor landscape has led them to seek out platforms that ‘centralize’ advisors – from broker-dealers to RIA custodians, IMOs to enterprise RIAs, advisor membership associations and networks to even other software vendors (e.g., portfolio management or CRM systems) that had a greater market share in an adjacent category – in the hopes of partnering together to reach a higher volume of advisors at once.

Yet the allegiances that have been formed from such distribution strategies, which cause certain software providers to integrate deeply with some advisor platforms and vendors but not at all with others, has resulted in a form of Balkanization of advisor software, where clusters of advisor software get along well with one another but are competitive with and hostile to other clusters of advisor software, even across categories and vendors that might otherwise complement one another but simply don’t have the resources to integrate to “everything” and therefore had to choose where they would (and would not) align.

Thus, for instance, even “independent” broker-dealers typically only allow their advisors to use certain vendors but not others, independent RIAs are often constrained to what technology vendors their RIA custodians choose to integrate with (or not), and advisors that rely on certain key systems as the hub of their business (e.g., Salesforce or Redtail or Orion or Tamarac) are constrained to what other technology solutions those ‘anchor’ technology vendors choose to integrate with (or not). For most advisors, even great technology that doesn’t integrate with their platform or hub may as well not even exist.

Who Are The Real Winners And Losers In Financial Advisor FinTech?

The balkanization of advisor technology companies over the past decade, with mini-ecosystems of solutions that form around centralized advisor hubs, has to some extent been a necessity for many that facilitated adoption (providing a pathway to key partnerships that can drive growth of new advisor users) but has also become an inhibitor (as software companies that concentrate into a particular segment or channel of advisors can unwittingly steer their roadmap so deeply into that segment of advisors that it is no longer even saleable to the rest!).

The broader challenge, though, is that the fragmentation of advisors and the consequent balkanization of advisor software has made it incredibly difficult to even understand which companies have market share amongst advisors in the first place.

Because the reality is that in today’s environment, certain advisor technology solutions have very high user adoption in the channels where they have distribution, but near- or outright zero adoption in other channels outside of their core. Such that understanding which companies are gaining (or losing) market share is highly dependent on which types of advisors in which channels are asked the question in the first place.

Consequently, today’s industry surveys of advisor technology often show wildly different market share adoption for key technology vendors (and sometimes even wildly different market share within the same survey from one year to the next), with results that vary tremendously depending on which particular industry channels are surveyed in the first place (e.g., surveys with a heavier sampling of RIAs show one pattern of market share adoption, those that sample more from broker-dealers show another), and none of which is necessarily representative of the advisor technology landscape as a whole.

Alternatively, in an attempt to expand their sample size amongst advisors, some industry surveys use “open” survey links that can be followed and clicked by anyone. The good news is that by widely sharing survey links, the number of participants often increases dramatically, producing some of the largest advisor samples. The bad news is that in practice, vendors themselves often push the survey links to their own users to encourage them to participate. Which turns a study on “which software solutions are advisors using” into more of a popularity contest driven by “which software vendors are most effective at turning out their advisor users to vote” instead.

All of which has created significant frustration for the advisor community itself. Because when it comes to seemingly straightforward questions, like “what is the most popular solution for X” or “what solution do advisors like the most for X”, there is no clear answer because most industry studies are not representative (and instead tend to be overly concentrated amongst a software company’s power users who took the internally promoted survey, or may have market share distorted by which industry channels the study did or didn’t sample in the first place).

Similar, venture capital and private equity firms that want to invest growth capital into the most successful up-and-coming AdvisorTech solutions also struggle to identify which companies are up-and-comers because, again, industry fragmentation and inconsistent sampling methodologies can obscure which companies are really gaining (or losing) market share, in which channels they are (or are not) growing, and whether their software is (or is not) well-received (and likely to grow by word of mouth) by the advisors who are using it.

The First Kitces Research Study On Advisor Technology

In light of the industry challenges in understanding what’s really working (or not) in advisor technology, we’ve decided at Kitces Research to conduct our own Advisor Technology study, and leverage our natural strengths – a nerdy team of PhD researchers, including Dr. Derek Tharp and Dr. Meghaan Lurtz, trained and skilled at designing effective survey methodologies to get a strong representative sampling of the advisor community.

Which means this Kitces Research study on Advisor Technology will be different than most. There will be no open survey links to share and distribute; instead, participation will be by “invitation only”, distributed through a combination of emails, phone calls, and even snail mail (yes, we’re really going to try to reach some advisors who don’t otherwise participate in industry surveys but have valuable perspective to share on what technology they’re using and what they like or don’t like!).

We will make further adjustments to correct for representativeness (as necessary) during the analysis and reporting process, recognizing that when wirehouse advisors (for instance) are approximately 15% of the total population of financial advisors, their technology usage results should reflect a 15% weighting in the final reporting of market share for what advisors are using (even if their actual participation in the study happened to be a few points higher or lower).

In the end, our goal with this Kitces Research study on Advisor Technology is to answer a few key questions:

1) What are really the most popular Advisor Technology tools (and how do they vary by industry channel, firm size, and other differences in advisor business models)?

2) Which Advisor Technology solutions are actually “good” (well-rated) by the advisor community?

3) Which categories of Advisor Technology have the most opportunity for growth (low adoption) or disruption (low ratings) where industry innovation could thrive?

By analyzing the advisor community broadly, we also hope to explore the dynamics of independent advisors versus large advisor enterprises (both employee and independent advisor platform models). Because long ago, enterprises had an edge when it came to advisor technology, as they had the resources to build the most deeply integrated technology systems. In recent decades, the pendulum has swung to the independents, powered by internet-based API-driven technology solutions into a thriving ecosystem of independent advisor technology so strong that even large enterprises increasingly now buy “independent” software. But with a recent resurgence of enterprises building their own solutions again – or even buying independent tools and turning them into their own – and the ability of enterprises to force (or manually build) their own deeper integrations (e.g., Commonwealth’s Advisor360, or RBC Black, or Merrill Lynch’s Advisor Workstation), could the pendulum be swinging back again towards enterprise advisor software?

As always, we’ll report the results back out to the advisor community. In the hopes of not only helping advisors themselves identify the best technology to use (in their advisory firms, whatever their particular needs), but also guiding advisor technology firms where they could focus their efforts more deeply, where growth investors should put their dollars to bring more capital to the advisor technology firms that could best deploy it for positive impact in the advisor marketplace, and where new advisor technology startups could potentially innovate to move the whole advisor community forward in the future!

In the meantime… please stay tuned for your invitation to participate in the Kitces Research study on Advisor Technology!

Leave a Reply