Executive Summary

Despite the ongoing shift to an increasingly digital world of automatic electronic verification of everything from transactions to identity, the reality is that today, there are still a number of documents that individuals must be able to provide to various companies, regulators, or government agencies. In some cases, those entities will at least accept digital copies of the relevant paperwork or supporting documentation, while in other cases “original” hard-copy versions are required. Which in practice has made it extremely difficult for many households to even figure out what to keep in physical form, what can be scanned and retained digitally, what can be discarded, and what must be shredded.

In practice, though, there is no hard-and-fast rule about what documents should be retained (or not). The process of figuring out “what to keep” (in physical or digital format) and “what to shred” depends on the nature of the document and what it will be used for.

For instance, tax documents generally only need to be kept for 6 years (the statute of limitations, even if there is a substantial misstatement of income), and under Revenue Procedure 97-22, such documentation can be retained entirely in digital (and not physical) format, as long as the scanned/photographed copy contains all of the relevant information.

On the other hand, documents pertaining to personal identification (e.g., Social Security card, birth certificate, and Driver’s license) must be kept in original physical form (and should be kept permanently), along with key legal documents (e.g., Wills and trusts and Powers of Attorney), in order to be able to help prove their authenticity.

When it comes to the documentation of assets and liabilities (from real estate or other ownership records, to credit cards, mortgages, and other debt), records must be retained as long as the asset is owned (or the liability is owed). Or in the case of documentation like insurance claims, as long as the claim remains open.

Storage of key documents in practice will vary by household, but important physical documents are typically stored in a home safe, a safe deposit box (though important legal documents should not be held there, as they may be necessary to access the box, which is impossible if they’re in the box!), or even the safe of an attorney’s office. For those that prefer digital storage (for documents that can be stored digitally), external hard drives and thumb drives have long been popular, although cloud-based solutions are increasingly popular (particularly for their redundant back-ups, and the ability with some systems to designate Trusted Contacts to access the information in the event the primary owner is deceased or incapacitated).

Ultimately, a checklist of key documents to retain (and how long to retain, and in what form) can be helpful as a way to be certain that all the important documents are covered. For financial advisors, this can actually be a pathway to reinforce value for clients, by actually going through such a document checklist with clients, helping them determine what to keep and what to discard, and even offering ‘shred-it’ days for clients to help them get their own financial households better organized!

As “social animals”, the systems that human beings have created and operate within are all built on a foundation of trust. It’s trust that when we go to a store and purchase something, the product will do what the company says it will do. It’s trust that when we pay for that item, the cash we’re spending is legitimate (and not counterfeit), or the credit card we swipe is really ours. It’s even trust that when we report our income at the end of the year for tax purposes, what we said we’ve earned (and what we said we owe) are accurate statements.

Of course, the reality is that trust alone only goes so far, though. As a result, while we generally trust what we purchase, government regulators and agencies do put additional consequences in place for businesses that engage in false advertising about their products or services. Credit card companies do have fraud detection systems in place to identify ‘questionable’ use of an otherwise-seemingly-valid credit card. And the IRS does audit at least a small percentage of tax returns every year… and strikes fear in far more that they could be audited (and be caught, and face consequences) if they violate that trust.

In turn, some transactions are so weighty that we can’t even operate on trust alone, and instead must provide documented proof upfront. Even in a digital world, there are often still requirements to provide copies of a Driver’s License, proof of birth or marriage or death, or substantiation of an item of income or expense or ownership.

Which means it’s necessary to retain copies of those key documents and records to be able to provide the relevant proof when the time comes. Except over the years and decades of our lives, that can cumulatively add up to a substantial number of financial and other key documents that must be retained. Which eventually raises the question of which ones really need to (still) be retained after many months, years, or decades have passed!

And the matter is only further complicated in the modern digital world, where it’s also possible to scan and retain a digital copy of a document (and throw away or destroy the original). Which just introduces even more questions, of not only what can be discarded and what must be retained (and for how long), but which records can be retained digitally versus needing to retain a physical ‘original’ copy?

And the stakes can be high. Failure to adequately store essential documents can have a serious negative financial impact. For example:

- Failure to maintain proper records can result in IRS tax penalties in the event of a tax audit.

- Several financial records are needed when applying for a loan. When documents are not readily available, a borrower may miss an opportunity to lock in a favorable rate, qualify for a mortgage, and/or lose out on making a desired purchase altogether.

- If the validity of ownership is ever challenged, deeds and other title documentation may be needed to prove legal ownership of an asset.

- In litigation or other legal disputes, defendants (or plaintiffs) may need certain documents to prove their case or claim. There may not be any other copies available, and the legal dispute could come down to an individual’s personal file organization to prove their case!

To further complicate matters, not all sources agree on the list of key documents and their retention periods. For example, the Federal Trade Commission suggests that W-2s should be retained for seven years (to cover the statute of limitations for an IRS audit), yet the IRS states that W-2s should be retained until someone begins collecting Social Security (in the event there is a correction needed to their Social Security earnings history to properly determine their benefits).

For some, the default response is simply to keep “everything”. But in practice, “everything” can become very cumbersome to keep over the decades of one’s working career and retirement (and even more challenging to retain in a manner organized enough to be findable if the document was ever actually needed!). For which the solution is to start purging no-longer-needed documents. Except it’s crucial not to eliminate the documents that might really have needed to be kept!

Which means ultimately, getting more financially organized starts with getting clarity about what actually does need to be kept, or not, amongst one’s financial (and other key) records, in order to ensure that what needs to be retained is retained (and is retained in the physical or digital manner that it needs to be retained)!

Retention Policies For Important Financial (And Other) Documents

Because different types of financial and other documents are used for different purposes – each of which may have its own rules and timelines depending on the context – there is no hard-and-fast rule for how long “key documents” in general must be retained. Instead, the appropriate personal retention policy depends on the nature of the document.

Key documents that have their own specific rules for what should be retained (and how) include:

- Tax Documents (e.g., W-2s, 1099s, and tax returns)

- Healthcare Documents (e.g., medical expenses)

- Legal And Personal Identification Documents (e.g., Wills, Trusts, and IDs)

- Ownership And Borrowing Documents (e.g., Deeds and Liens)

- Other Specialized Documents (e.g., College Transcripts, Military Records, and Insurance Policies)

How Long To Keep Tax Documents

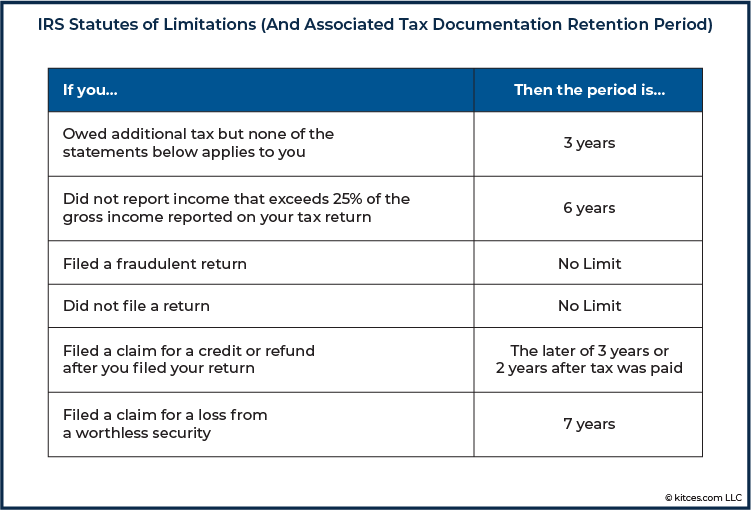

Generally, households should retain copies of their income tax returns for at least three years, in accordance with the general statute of limitations for the IRS (which allows it to go back 3 years in an audit).

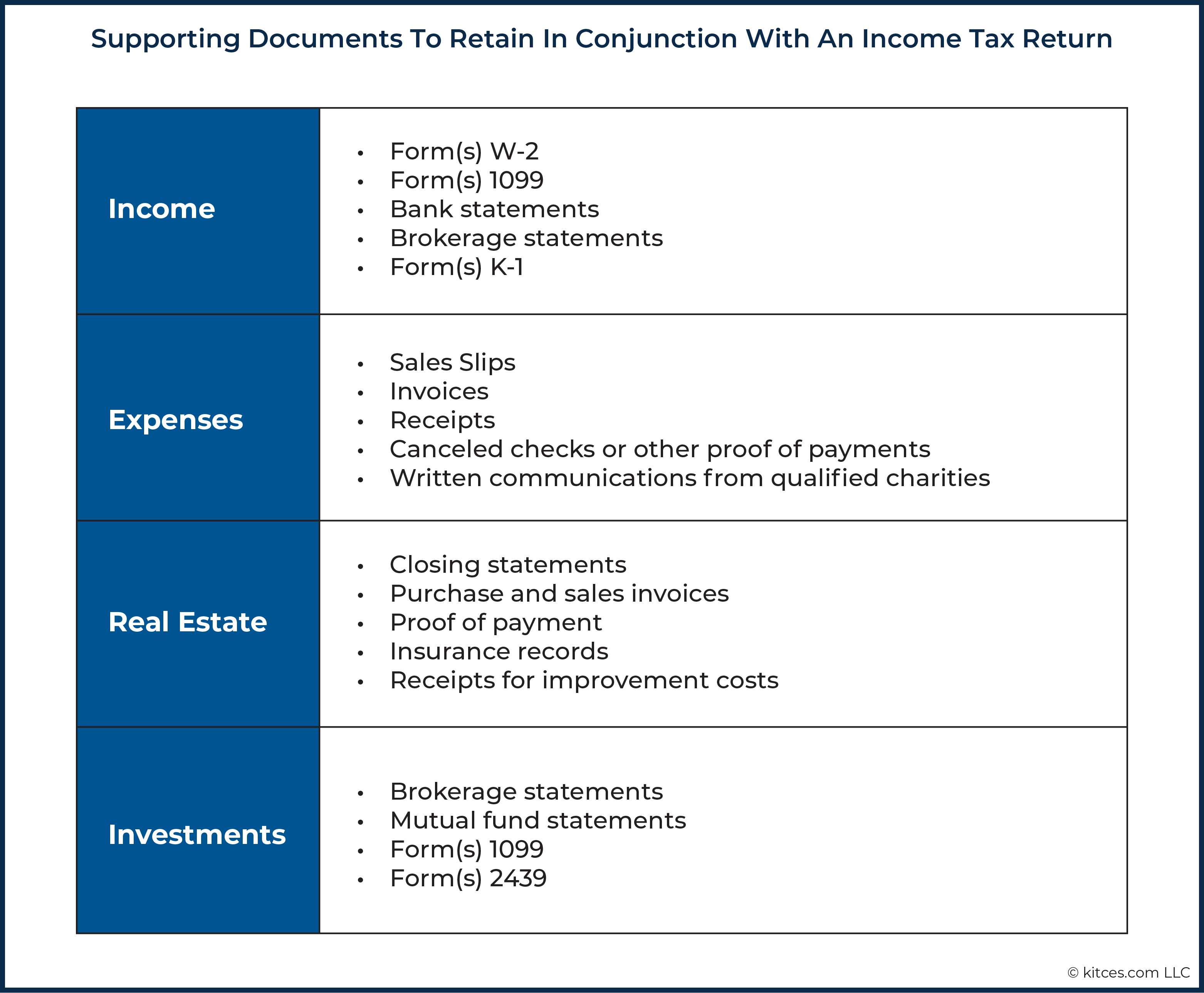

Notably, though, it’s not just the tax returns themselves that must be kept on file, but also any/all supporting documents that were used to arrive at the figures (income or expenses) reported in the returns. The chart below outlines the types of supporting documents that should be retained along with an income tax return.

However, it’s important to understand that there are many exceptions to this three-year statute of limitations (and the associated period to keep tax records).

For instance, in the event that there is a substantial misstatement of income, the statute of limitations is extended to 6 years, which is arguably a better baseline for retaining tax documentation. And if a claim is filed for an investment that was deemed worthless (not just sold for a loss, but written off entirely as a total loss), the statute of limitations (and suggested retention period for any documentation associated with the worthless investment that was ‘abandoned’) is 7 years.

And of course, if a tax return is never filed in the first place, the IRS indefinitely retains the right to ‘challenge’ the failure to file an income tax return that year (which means by definition there may be no tax return to keep, but other tax documentation that year, if only to prove there was not enough income to merit filing, is still recommended).

Accordingly, the IRS’s Recordkeeping for Individuals (Publication 552. Revised January 2011) recommends the following:

It’s also important to consider each individual state’s requirements as well, and how far back they can look to audit state tax returns. For example, Arizona, California, Michigan, and Wisconsin’s statutes of limitations to audit tax returns is 4 years, while most states are only 3 years, though South Carolina will (similar to the Federal government) extend up to 6 years in the event of a substantial misstatement of income (if total taxes are understated by at least 20%).

Yet while 6 years (or 7 in the event of writing off worthless securities, which is the baseline recommended by the Illinois CPA Society) should be very safe for the retention of income tax returns and related documentation (at least, as long as a return was actually filed, and there is no outright tax fraud), there are several other tax forms (and supporting information) that should be retained longer or even permanently. For example:

It’s also important to note that the IRS has made it clear under Revenue Procedure 97-22 that digital copies of tax returns and the supporting documentation are acceptable. One does not need to keep physical copies of previous tax returns as long as there is a digital copy that is an “accurate and complete” replication of the hard copy.

Keeping Healthcare Documents And Medical Expense Receipts

When it comes to healthcare documents and the receipts for medical expenses (and their associated reimbursements), the retention of records again depends on the context.

The primary reason that records of medical expenses (and associated insurance reimbursements) are kept is to substantiate any deductions for medical expenses. In practice, though, if medical expenses were written off on the tax return, then these medical expenses would be treated as supporting tax documentation and should be retained as long as the individual must retain their tax return records (generally, 6 years). Notably, this also means that a digital version of such receipts would be sufficient.

On the other hand, one popular tax strategy for Health Savings Accounts is to pay medical expenses initially out-of-pocket while contributing to an HSA, and then later taking distributions from the HSA (after years or even decades of tax-free growth) to ‘repay’ oneself (and/or using the HSA as a supplemental saving vehicle for retiree medical expenses). As long as the individual has kept a record of who they paid, the amount, and the date the payment was made, the strategy is permitted. Though doing so means that as long as there is a balance in the HSA (and any expectation of wanting or needing to rely on prior medical expenses to validate future HSA distributions), documentation of qualified medical expenses should be kept (even if for years or decades), though again digital format is permissible (per standard IRS policy on tax documentation under Revenue Procedure 97-22).

When it comes to keeping documentation of medical expenses simply to make a claim for insurance purposes, the documentation retention period is either the maximum time period to submit for a claim or reimbursement (which may vary by insurance carrier, and insurers may vary on whether they accept digital or only hard-copy documentation), or for a claim that has been submitted, until that claim is paid and the insurance company reports it as closed. After which the detailed expense documentation is a moot point and can be disposed of, if not otherwise needed for the aforementioned tax purposes or strategies.

For those on Medicare, it is suggested to retain their Medicare Summary Notice for at least one year. Since this is mailed out every three months, the individual should plan on keeping the four most recent Medicare Summary Notices on hand. And, if they are enrolled in a creditable employer drug plan, they should retain the most current “Notice of Creditable Coverage”, which would be needed when the individual enrolls in Medicare Parts B and D to avoid paying any Medicare Late Enrollment penalties.

Retaining Legal Documents And Personal Identification Records

Key legal documents, including important business records, substantive personal transactions, and the core components of an individual’s estate plan (including the most current Will, any trusts, general and healthcare Powers of Attorney, a living Will, and any beneficiary designation forms) are some of the most important documents for households to retain in their own files. In practice, many will keep such documents in a home safe for further safekeeping (though a safety deposit box is not recommended, as heirs may not be able to access the legal documents in the box without the documents to prove they have permission to access in the first place!). Alternatively, some may keep copies in their attorney’s files as well (or even as originals in a law firm’s safe).

Because key legal documents – particularly key binding contracts – are also a document that may need to be not only produced (to ‘document’ a transaction) but also substantiated (i.e., that it is not fraudulent or forged), legal documents that were not formally and legally “e-signed” should be kept as physical paper copies (and not merely scanned to retain a digital copy).

In addition, if the individual is married, copies of the marriage certificate should be retained permanently, along with any prenuptial agreements (should also be retained permanently). If the individual has gone through a divorce, they should keep copies of the official divorce paperwork as well, including the written separation agreement and all other orders and decrees. If the individual was widowed, they should still retain their late spouse’s death certificate, and all estate settlement paperwork indefinitely (in case there is ever a need to prove that the estate was in fact settled, and that there are/were no reasons to contest the Will).

There are also several key personal identification documents that can be grouped together to prove citizenship and birth. Each of these must be kept permanently. They include a Social Security card, birth certificate, and the (most current) passport. For parents, it is important to ensure that the document retention policy includes the important documents related to their children as well (including adopted children).

Several important documents are associated with owning assets and having debts. At its core, “documentation” can not only substantiate ownership itself (i.e., proper records can help to prove ownership in case ownership is ever challenged), but also the terms of ownership or commitments (e.g., the terms of a purchase or a loan).

Documentation of assets and debts also helps to track pertinent information about those assets and debts over time, from the balance/value/performance of the holdings, to their cost basis for tax purposes (in case the IRS audits a tax return).

Because different types of assets and debts have different characteristics, the associated document retention obligations are different. The three core categories of documentation for assets and debt include:

- Intangible Assets

- Tangible Assets

- Liabilities

Intangible Asset Document Retention

Intangible assets are those for which we contractually have “ownership” but there is no physical, tangible manifestation of the asset. Most commonly, this includes various types of financial (e.g., bank or brokerage) accounts, though it may include other types of property (e.g., intellectual property in the form of patents or copyrights).

Proving ownership of a bank or brokerage account is typically not necessary – it is the job of the financial institutions to hold such accounts on behalf of their customers in the first place – but the tax consequences of the investments in those accounts (as they grow or are bought and sold) do necessitate that documents be retained, in particular, to prove out cost basis.

Accordingly, investors that own investment accounts have a few different records that they should retain:

- Current statements should be kept on file for that particular year, but can typically be disposed of at the end of the year (in lieu of an end-of-year summary statement)

- The End of Year statement (or December statement) should be retained in conjunction with the supporting tax records (typically 6 years).

- If investments were purchased prior to 2012, the investor is responsible for maintaining and documenting cost basis records (and reporting accordingly to the IRS when sold). Investments purchased in 2012 and later will have their cost basis tracked by the financial institution, which automatically reports the cost basis on the 1099 when sold.

Notably, the irony of the current cost basis tracking rules is that maintaining statements after 2012 to prove cost basis is no longer necessary, but pre-2012 end-of-year statements are valuable to retain to document cost basis until all such investments have been sold. As the IRS 6-year statute of limitations for tracking the tax consequences of an investment sale don’t begin until the investment is actually sold (which means retaining documents that could stretch years or decades prior for an investment that has been held for a long time!).

Fortunately, though, “documentation” for cost basis purposes again does not require the original physical statement as proof; a fully intact digital copy is sufficient in normal circumstances. As a result, it is permissible to scan prior investment records (and trash/shred original paper copies).

Tangible Asset Document Retention

Tangible assets are “real” physical assets – from our furniture and other household goods, to more commonly (from a documentation perspective) our automobiles and real estate. Which come with their own important documents that must be retained.

In the context of tangible assets, proving ownership is rarely an issue, but can be a substantive one if and when it does occur. As a result, individuals should keep any documents related to the ownership of the property until it is eventually sold. This includes any deeds, titles, settlement statements, or bills of sale.

From a tax perspective, it’s also important to document any expenditures associated with tangible property (particularly real estate) that may contribute to the cost basis of the asset. Accordingly, documentation of any expenditures for substantial improvements to the real estate, along with documentation of any transaction-related fees that were capitalized when purchasing the property, should be retained until the property is eventually sold.

When it comes to homeownership (i.e., our primary residence), it is similarly important to retain documentation of any home improvements that may affect the cost basis of the house which could result in reducing the tax liability when it is eventually sold. These records should be maintained throughout the ownership of the home.

However, there are a few additional circumstances where documentation may be necessary (and documents should be retained):

Debt/Liabilities Document Retention

When it comes to those who are carrying debts, the primary issues of documentation are being able to substantiate the terms of the loan (e.g., payment obligations, interest rates, etc.) and when the liability has ultimately been extinguished.

Accordingly, it is important to keep any loan documents or borrowing agreements on hand until the loan is paid off. Once the loan is paid off and a notification has been provided that the debt is extinguished, it is no longer necessary to retain any documentation (though in practice it may be desirable to retain documentation that the loan has been paid off).

Other Important Documents To Retain

While not specifically covered above, there are a few other important documents to keep on file.

College transcripts and higher education records (such as a certification) should be retained to prove that the course work was completed, in addition to the associated educational expenses themselves. In many cases, expenses related to education may afford you, the individual, certain tax credits and deductions when filing the tax return. After the (generally 6-year) retention window for tax-related documents, though, maintaining college transcripts and other proof of education is generally unnecessary, as such documents can most likely be (re-) ordered directly from the educational institution. However, it may be helpful to retain documentation in case the institution fails to properly retain records (or the educational institution itself ceases to operate!).

Insurance policies (including homeowner, auto, health, disability, and life insurance) should be retained for all current policies. While replacement policies can typically be obtained directly from the insurance company, because insurance policies are ultimately legal contracts, they should be retained as long as they are relevant (i.e., in force as insurance) like any other legal document.

For those who have previously served in the military, it is important to retain copies of discharge papers to prove future eligibility for veterans’ benefits.

Finally, for those who are employed and signed a non-solicit or non-compete agreement, it will be very important to retain a copy for the entirety of their time with that employer, and for the subsequent years that the agreement covers following their departure.

Checklist Of Important Documents To Keep

Because many key documents are situational to the individual’s circumstances about whether the document would even apply, and the context in which is it being held (e.g., documentation to validate that the residence is owned, or simply to substantiate the cost of improvements for cost basis purposes), in practice “what documents an individual should keep” is a matter of considering all the situations in which document retention may apply.

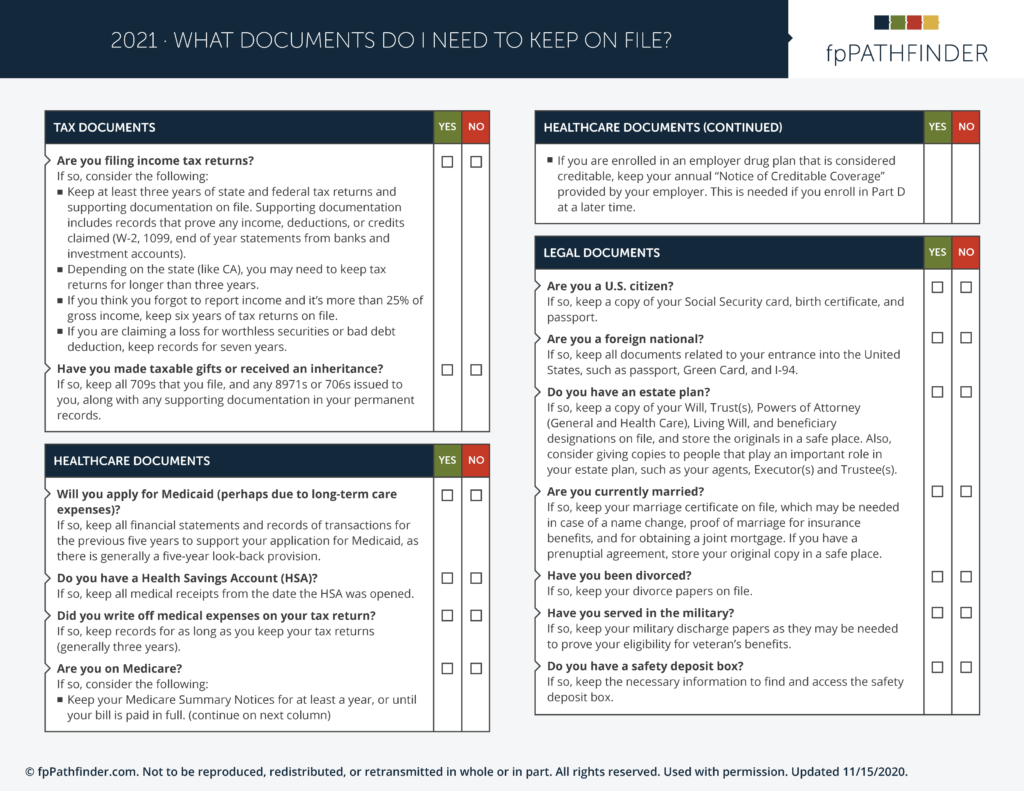

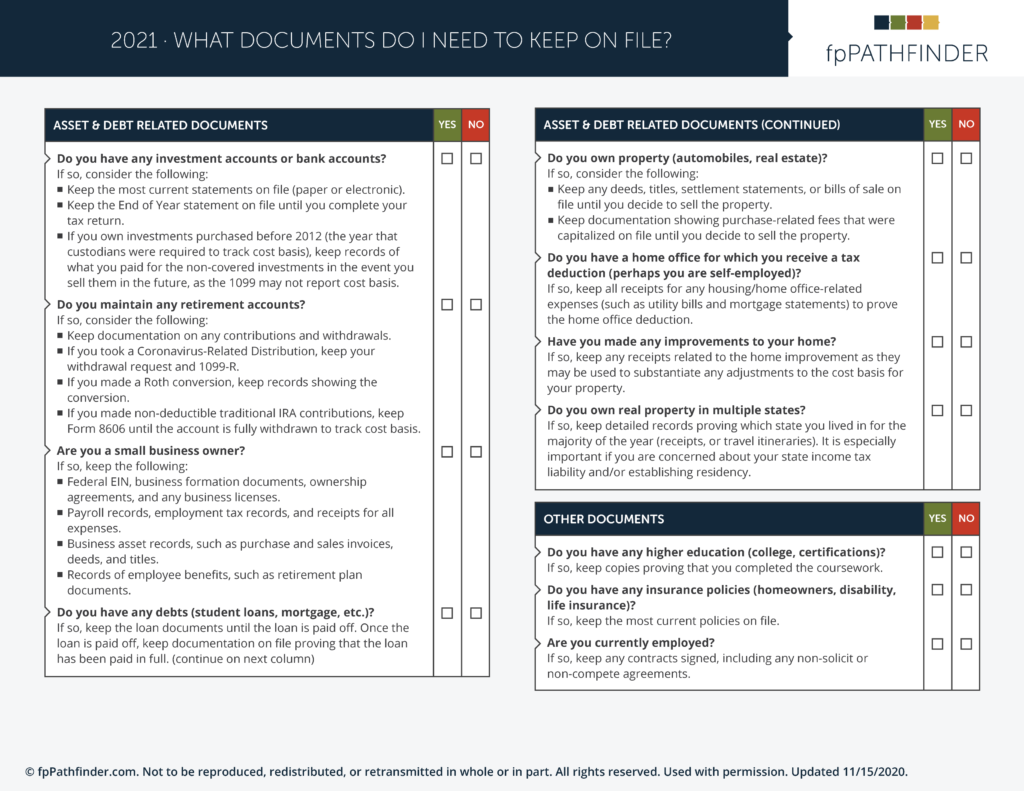

The checklist below on “What Documents Do I Need To Keep On File?” provides a summary of the key information.

Best Ways To Safely Store Important Documents

With the important documents pulled together, the next step is to properly store them. There are a few different considerations to make at this point.

Depending on personal preferences, there may be an inclination to keep virtual records of important documents versus physical versions. In reality, some records can still only be stored physically, so any document retention policy should include steps for handling virtual and physical documents as most households will end out having a mixture of both.

There are no set standards as to what documents can safely be retained virtually. While the IRS has stated that digital records are acceptable, some government agencies (such as some state DMVs, like Connecticut’s DMV) and businesses (like certain insurance companies) may still require original (physical paper) documents.

For either option, unique circumstances must be considered.

Virtual Document Storage Considerations

For those who do want to convert physical documents to a digital format for retention purposes, it’s necessary to consider both how to digitize documents, how to store digital documents, and ultimately how to dispose of digitized documents if/when they no longer need to be retained.

Document Digitization: After collecting the important documents to be retained virtually, the first step is to begin actually digitizing them. Notably, while over the past two decades most people have used scanners to turn physical documents into digital ones, arguably at this point a physical scanner is no longer needed to scan important documents. There are numerous smartphone apps that can capture clean and precise scans of documents just as well as traditional scanners. Though for those who want to convert a significant number of documents from physical to digital, a desktop scanner may be appealing if only to be able to leverage an automated document feeder to go through a large stack of papers at once.

Digital Storage of Documents: Once scanned, important documents can be stored in a number of different locations, which can ultimately be categorized into two broad types:

- Personal Storage Devices. Storing the files on a personal computer, thumb drive, or external hard drive that physically remains in the individual’s possession. The benefit is that the information can be well organized (by whatever file folder or other organizational approach desired), and does not take up nearly as much physical space compared to having physical copies of all the important documents. The downsides are that the digital files could still be damaged (e.g., if the hard drive fails), or the storage device could be stolen. If this is the option that is chosen, consider using third-party encrypting software to add an additional layer of protection in case the files are stolen. Also consider redundant backup options.

- Cloud Storage Systems. For those who are comfortable uploading their important documents to the cloud, services like DropBox, Google Drive, and Microsoft’s One Drive, along with a number of other popular cloud-based storage systems, are available, as are password management tools like LastPass. For clients of advisors, there are also document vaults connected to some financial planning software (e.g., eMoney’s Vault), portfolio management software (e.g., Orion), or advisor-client file-sharing services (e.g., ShareFile). The benefit of this approach is that the documents can remain in the cloud, with the protection of robust backup and security protocols (as cloud service providers typically have far more depth of backups and storage redundancies than a typical personal hard drive stored in one’s home) to ensure client documents are properly protected. From the advisor’s perspective, advisor-driven document-sharing services also facilitate sharing more easily when the client needs them, and in some cases, like eMoney’s Vault or EverPlans (or for consumers directly, LastPass Emergency Access), the advisor or a trusted contact can access some of the documents in the event of an emergency.

Digital Document Disposal: Deleting digital files is generally a straightforward process, with one exception. There is a distinction between “Delete” and “Permanently Delete.” Depending on the storage system used (external hard drive or cloud storage), the file must be deleted and then deleted a second time. Oftentimes, the user will be prompted to confirm “Permanently Delete.” The purpose behind this is to allow users to have the ability to recover their files even if they deleted them – which is helpful if a file is accidentally deleted, but not good for those who want to delete files and not risk having a thief recover the file from a stolen hard drive. Permanently deleted files cannot be recovered in the future.

Physical Document Storage Considerations

When it comes to maintaining physical documents for storage – particularly those legal documents that must be maintained in original physical form – it is again important to be mindful of both how the document is stored, and how it is disposed of when it is no longer necessary to store.

Physical Document Storage: For important documents, there are two types of storage systems that should be considered:

- In-house storage: This can provide a high level of protection, but for the most important documents that must remain secure, it can be expensive. As while many people prefer to keep physical documents on hand to keep them “safe” – potentially even in an actual physical safe – keeping physical documents on-site requires protecting them against the three most common perils: fire, water, and burglary. Especially recognizing that victims of a burglary may simply find that the entire safe is stolen (in other words, the burglars don’t try to break into the safe to steal the documents, they steal the safe itself and get the documents out later!). In addition, documents that “must” be retained are also at risk for natural disasters – in particular, fire (e.g., if the home catches fire) or water (in the event of a flood, or water damage from extinguishing a fire!). As a result, the most important documents that are stored at home need additional safe precautions (e.g., Wirecutter’s top reviewed safe, Honeywell 114 Lightweight Fire and Waterproof Chest).

- Safe deposit box: This provides a physical place to save important documents outside of the individual’s home (to avoid the need to take additional precautions against burglary, fire, and water). While there is a fee for this service, some may prefer this over a safe in their home, as it may provide a higher level of security (and/or at least do so at a more favorable cost). If this option is selected, it is important to share information regarding the location of and access to the safe deposit box with trusted contacts, so it is not lost in the event that the original owner is unexpectedly incapacitated. Also, note that certain original documents should not be stored in safe deposit boxes (e.g., Wills and POAs) because the executor may not be able to access the safe deposit box until they can prove they are the executor or have a power of attorney (which they cannot do if the documents are in the safe deposit box in the first place!).

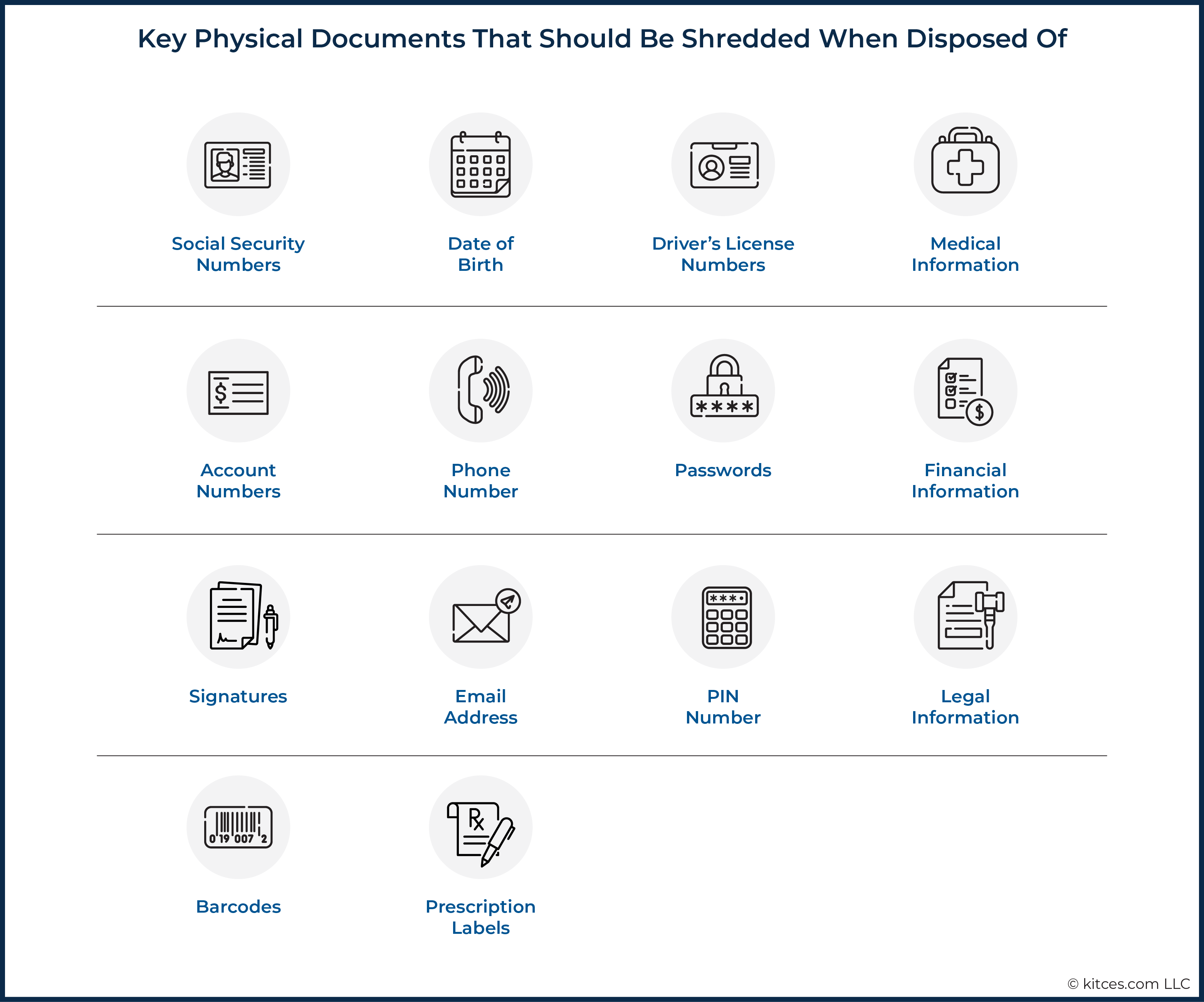

Physical Document Disposal: When it’s time to dispose of important documents, shredding may be the most straightforward approach. It ensures that no one can view the information after it has been discarded. There are key pieces of information in many of these documents that criminals can use to steal a client’s identity. Below are some examples of sensitive information that, if listed in the documents, should be shredded:

Getting Started With Document Retention

In practice, implementing best practices in document retention often serves as an opportunity to get organized in the first place. In turn, for financial advisors, having a conversation about document retention is an appealing opportunity to help clients get their records in order.

Accordingly, there are a few different strategies that advisors can consider implementing with clients to get them organized (and keep them organized going forward) with a focus on document retention.

Initial Document Retention Policy Establishment

At least initially, the process of creating a document retention policy can be time intensive, since each client will have a unique list of documents that they will need to retain. Though in practice, helping clients to “Get Organized” can actually be an alternative approach to the data-gathering meeting, helping clients to organize their files, implement best practices in document retention… and digitally capture key documents and information along the way for the financial advisor.

At least initially, the process of creating a document retention policy can be time intensive, since each client will have a unique list of documents that they will need to retain. Though in practice, helping clients to “Get Organized” can actually be an alternative approach to the data-gathering meeting, helping clients to organize their files, implement best practices in document retention… and digitally capture key documents and information along the way for the financial advisor.

As in reality, clients may feel guilty that they don’t have all these important documents already organized, or simply won’t be willing to make the time if it is not structured for them.

Ongoing Document Retention Policy Maintenance

After a household has gotten properly organized for the first time, now begins the ongoing task of staying organized. There are a few strategies to consider.

For high-touch advisory firms, there is an option to keep the client organized during the year. Perhaps an intern or administrative assistant could scan or file the new/updated important documents and shred the ones that are no longer needed for retention purposes. Similarly, advisory firms could maintain a shredder (or a shredding disposal unit) in their offices and remind clients who are coming in to bring any documents to shred.

Alternatively, the advisory firm could simply provide a list of documents to update and remove on a regular basis (e.g., as a newsletter email sent to all clients, or an annual agenda item to review once per year), or implement a standardized checklist template with clients to establish their own document retention policy of what to retain and for how long, and periodically review.

It may even be helpful to leverage certain times of year, like World Backup Day (March 31st) or Records and Information Management Month (April), to promote to clients and offer resources to assist in document organization. For example, the advisory firm could host a yearly shred-it day, where clients could bring in old documents to be shredded at the end of April.

Document management is really important, and yet oftentimes, households are not organized, and/or are unprepared to be able to find and access documents when they’re really needed. It’s no fault of the individual because, in practice, the rules over the years have been vague, inconsistent, and in flux. With some oversight and guidance though (and a value-add opportunity from the advisor themselves!), households can be better organized and better prepared to handle future events that may require supporting documentation.

Leave a Reply