Welcome to Retirement Scan, our daily roundup of retirement news your clients may be talking about.

Financial surprises retirees (and those about to retire) must avoid

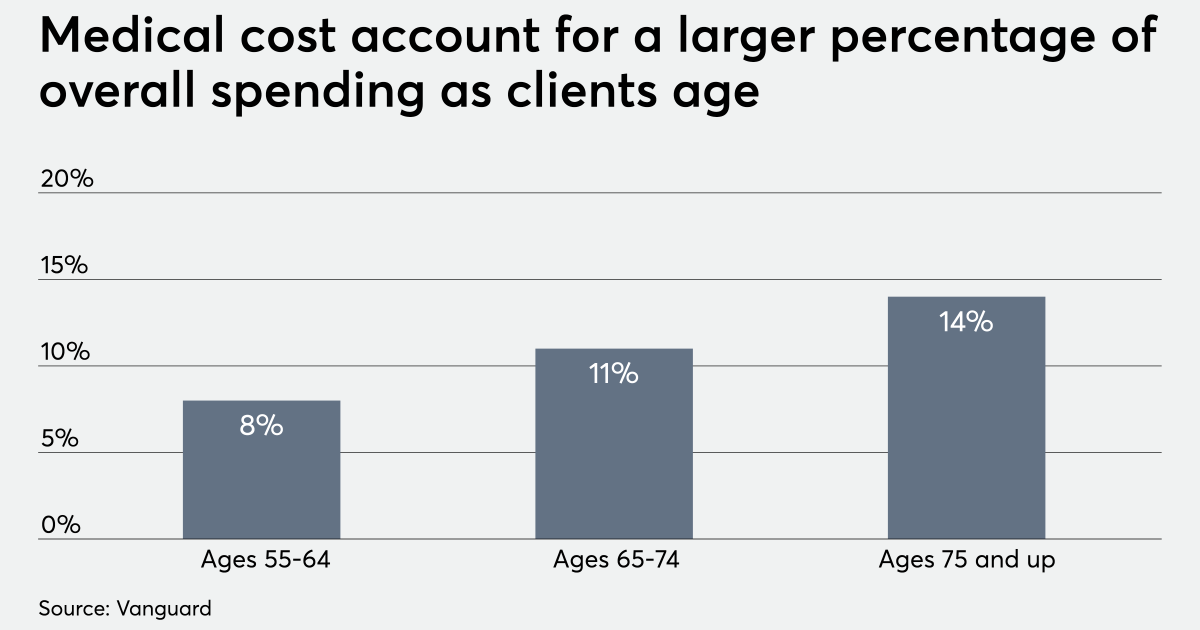

Retirees must be prepared to handle a wide array of potential financial surprises that could catch even the most prepared seniors in retirement off their guard, according to this Kiplinger article. For example, clients may find that the costs of Medicare and long-term care are higher than anticipated or their savings are shrinking at a faster rate. Those who retire early would also find health care to be very costly and might not get the expected savings after they downsize.

Why clients should consolidate those 401(k)s and IRAs

For a more efficient method of managing their savings in retirement, clients are advised to consolidate their 401(k)s and IRAs rather than owning assets in multiple, separate accounts, according to this CNBC article. Second sentence: Withdrawal rules vary for 401(k) plans and IRAs, and failing to comply could trigger tax penalties, according to the article. “The more accounts, the more choices, and it’s cognitively more difficult for human beings to deal with. I think that’s really the basic issue,” according to a retirement expert at The Pew Charitable Trusts.

A guide to retiring in 2020

There are various factors clients must consider when planning for retirement this year, this article in Motley Fool addresses. Topics including health care, inflation, Social Security and annuities should be top-of-mind, according to the article. Clients who want to engage in retirement planning this year are also advised to seek professional advice, know the non-financial side of retirement and minimize the tax bite on Social Security benefits, distributions from retirement accounts and income from investment portfolio.

Do your clients’ kids need a Roth IRA?

Financial advisors should encourage their clients to set up a Roth IRA for their children, according to this article in U.S. News & World Report. Contributions to a Roth IRA are made on an after-tax basis, but investments and withdrawals are not taxable in retirement. Young clients can also dip into their Roth savings early without any tax or penalties, giving them flexibility when saving for future expenses.

Leave a Reply