Executive Summary

In the wake of the Coronavirus pandemic, many financial advisory firm owners are facing tremendous uncertainty about the future of their businesses. And even those business owners who have planned ahead for cyclical downturns may still have to make hard choices about how best to navigate the current turmoil and ensure the long-term survival of the business.

In this guest post, Angie Herbers – Chief Executive and Senior Consultant at Herbers & Company, an independent management and growth consultancy for financial advisory firms – walks advisors through six steps of crisis management that they can use to cope with the unique crisis we are facing today. Because the truth is that even for experienced advisors who have been through market turmoil in the past, each crisis is different (posing unique challenges to firms at different stages in their growth), and in practice, the biggest risk to an effective crisis management response is one of “false equivalencies”, in which an advisory firm owner makes the assumption that the current crisis can be dealt with in the same manner as the last. In fact, while financial advisors may plan for aspirational growth, few businesses actually do the planning necessary to ensure they can maintain the stability of their business in the event a severe crisis turns into a protracted one.

Accordingly, there are certain steps an advisor can take to ensure their crisis management strategy is specifically tailored to the current situation at hand, and the risks that loom in the event that it does not recover quickly. The first step is an assessment of the specific crisis that needs to be addressed right now (which, in today’s environment, is the health pandemic crisis more so than it is the financial crisis) so that the advisor can focus their efforts on the right problem. This is followed by step #2, consisting of a SWOT analysis to identify the specific threats to their firm and its culture (without which, employees will leave after the pandemic passes, and just plunge the business into another crisis!) and how those threats might best be addressed. The third step is about continuity planning, and why flexible compensation and partnership pay structures are critical to maintaining resilience in times of extreme uncertainty. Next, engage in financial stress tests for the business, recognizing that stress tests that examine stability, focusing on capital allocation and cash flow instead of growth rates and profit margin, are more relevant than aspirational or functional stress tests during times of crisis. From there, it’s time to engage in strategic planning about what firms will do to fix (and prevent) the specific problems many firms are probably facing in today’s tumultuous environment. And the last step is implementation, in which strategies are implemented with a focus on the firm’s culture, clients, and long-term organizational stability.

Ultimately, the key point is that financial advisors, like many other business owners facing hard choices in light of the current crisis situation, can take a course of action to respond to their situation, and if the right choices are made with the intent to protect the culture of the business (as well as the employees entrenched in that culture) over everything else, chances are that the business will survive this crisis, and will be positioned to grow even stronger and better equipped to face the next crisis. But the starting point is to be ready and willing to make the hard choices necessary to ensure the business survives and has the opportunity to thrive in the long run!

This article is not one I wish to write; the feeling is fitting, though, because this article is about dealing with hard things. The hardest part of running any business, including a financial advisory business, is dealing with financial performance when situations turn south.

While most business owners project their budgets, growth rates, and profit margins for aspirational growth, few businesses plan and run numbers for times of crisis. But a crisis is where we find ourselves right now, and financial advisors need to make the best decisions they can about the hard things when the numbers don’t go the direction they want them to go.

There is, at some level, financial uncertainty in our businesses and our lives every single day. When we encounter financial uncertainty, what we’re really running into is a problem and in cases where the problem is large enough, it can become a crisis.

I’ve been consulting with financial advisors for twenty years, so Herbers & Company is no stranger to crisis situations. We have gone through major downturns in the market with clients, we’ve helped advisors through Hurricanes Katrina and Sandy, wildfires in Colorado and California, and we have also helped them deal with the unplanned deaths of owners and leaders.

In addition to working alongside our clients in crisis situations, Herbers & Company has gone through major crises of our own: a tornado went through our business, two key employees passed away, and we experienced a failed merger.

We’ve learned a lot about what to do in crisis situations throughout these experiences. But here’s what you learn in crisis management and leadership training: the first rule of crisis is that every crisis is very different. While you can learn crisis, leadership, and management principles to help you navigate a crisis, the greatest risk to any crisis response is assuming false equivalencies. In other words, comparing today’s crisis to the last one you were in, and assuming you know how to deal with it already.

And this is because of the fact that every advisory firm today is dealing with a different set of variables—not just with financial numbers, but also with the people involved. This crisis, like every crisis in the past, is different than the last. The decisions change each day, with a different set of variables and actions to work through. Just a month ago, the US government asked us not to buy masks, now it’s recommended. In crisis, change happens rapidly, and how you respond to that change defines you one, two, three years – and sometimes even forever – into the future.

This article is written to help you think about what you are dealing with today. It’s not designed to give you answers; instead, it is simply written to help you think more deeply about what you are going through. Hopefully you have trusted advisors, attorneys, accountants, and consultants who can help you through it all.

To begin, and before you can ever think about the financial numbers of your firm, you first must recognize what is truly important in your business … in this crisis.

What Financial Advisory Firms Need To Understand About Crisis Management

From Herbers & Company’s perspective, the most important consideration in this crisis for financial advisory firms is preserving and evolving advisory firm cultures.

While this article is meant to help you walk through decisions about your numbers, my hope is you will not look at your culture as only a number. Rather, you will look at it as something you must preserve at all costs, because your culture is your people, and your people are more than numbers.

I have observed, in this crisis, that advisory firms are avoiding asking themselves the hard questions that they need to consider when business planning in this crisis. In other words, they are not allowing themselves to think about questions like these:

- What if the markets turn south for a prolonged period of time?

- What if we experience declining revenues rather than growing ones for a prolonged period of time?

- What if one of our employees gets sick and dies?

- What if I get sick and die?

The trouble is, by not dealing with the hard questions during good times, you run the risk of making bad decisions in a crisis that can cost you substantially in the future. At Herbers & Company, we prepare all our clients for the hard times. We do this because it’s logical.

Most independent advisory firms today get compensated on an Assets Under Management (AUM) fee structure, and many firms need to be able to sustain a drastic reduction of those fees at any time. This is because we simply don’t have control over the markets.

To prepare our clients, we run financial stress tests to ensure they have enough capital on hand to survive a major drop in revenues, and manage the inevitable negative cash flows. While many advisory firms look at profit margins as a buffer and the first line of defense in a downturn, Herbers & Company looks primarily at capital allocation and cash flow modeling.

Capital allocation—financial and human—in time crisis is often about redistribution of planned programs. For example, in the case of financial, you may have planned to upgrade your portfolio management technology and instead we’d reallocate that capital to client communication programs. Or you might be spending, say $2,000 on paid content for your blog, and we’d cut that cost and instead hire a $600 ghost writer, etc. In the case of human capital, you might have an associate advisor that we’d move to the back office to update client financial plans faster for lead advisors, delaying training to work with clients. There are thousands of different variations on how to redistribute capital, and advisors should be considering all their options.

In the case of cash flow modeling we’d project falling growth rates, while maintaining cost of employees and overhead expenses, minus debt payments and shareholder compensation, considering cash on hand. In other words, how long can the business last if month-to-month cash flow was negative but compounding cash flow stayed positive? The future cash flows in crisis become paramount and therefore, we need to know how long they last before we start tearing down structures already built and/or in the case of human capital, laying off talented people already hired. We do this before we think about growth or profits, because slashing employees and expenses can tear down what has already been built losing years of work.

Six Steps of Crisis Management for Financial Advisors

In order to stress test in turbulent times, you need to follow the six steps of managing a crisis. These steps help you determine if a crisis is major or minor, and then guide you through how to react to it financially.

Of course, most often you will intuitively know whether a crisis ranks as major or minor on the crisis scale, but whenever a situation needs your full attention, this process will guide you through an actionable strategic plan for your business.

- Step One: Assessment. Identify (or predict) the type of crisis in which you find yourself or you believe may be coming. Is it major or minor? Most business owners run this assessment naturally, in their heads, based on news, government action and economics and/or what is happening in their businesses at the time. A good example is a hurricane. You know a hurricane is coming, so you start crisis management.

- Step Two: SWOT (Strengths, Weaknesses, Opportunities, Threats) Analysis. Look at your firm and understand your major Strengths, Weaknesses you need to fix, Opportunities to move out of the crisis, and list any major Threats to the organization. If you decide you’re running into a major threat that can’t easily and quickly be addressed, you need to go all the way through the following next four steps (whereas in cases where a threat is minor, you’d simply address the problem to solve it and continue business as normal).

How to determine if a threat is major is not always obvious. Business owners rely on and trust their own judgment when running their business, and they tend to get comfortable with the uncertainty of being wrong sometimes. The COVID-19 crisis is an excellent example. It is very clear that RIAs and industry partners viewed COVID-19 as a major threat. The COVID-19 virus news coverage started getting attention late November 2019, buried in the headlines.

If you go backward and read the trade publications, some RIAs did major pivots in late 2019 and early 2020. Coincidence? It’s not. Knowing the major threats and acting quickly gives you a competitive advantage in a crisis on all fronts.

Not all crises are natural disasters, like COVID-19 and hurricanes. There are many threats to an advisory business, but you must watch for them. Once you determine a threat is major, you need to go through the following four steps … fast and steady.

- Step Three: Continuity Planning. Without a continuity plan to guide your reaction to major threats, you create more crises to deal with and compound your problems. Not having a continuity plan creates a “crisis of continuity”, which may turn into a brand crisis, people crisis, client turnover crisis, technology crisis, regulatory crisis, etc. At this point, if you have a continuity plan, you start working through it.

For those firms who don’t have a continuity plan, you must quickly create one. And, I might point out, when you are working in a regulated industry, you do not want to get stuck in a major crisis without a continuity plan. Therefore, any firm operating without a continuity plan is always in a major threat until it’s done and tested.

- Step Four: Stabilize Cultures and Operations. Ensure the safety of your team by communicating with them about the crisis and soliciting their involvement in helping you manage it. After you’ve asked for help from your team, you need to run the right financial stress tests on your business, so you can gauge the stability of your business and let your people know that the company is (or will be) prepared to weather through the crisis, come what may.

- Step Five: Strategic Planning. At this point, you’re ready to deal with any hits to your firm’s financial performance and culture. Here, you’ll look at your balance sheet first, not your P&L.

As I explained above, we first need to know how long you can sustain a hit to your numbers because, in a major crisis, and especially a natural disaster, you have little control over growth in your business to overcome losses in top line revenue and profits. This means capital allocation and cash flow modeling is more important than revenues and profits because we need to know how long you can go before your future cash flow goes negative and you have to dip into you savings to survive.

As you know, making financial decisions in crisis situations can be emotional, not sound. As a leader, your job is to make sound decisions for your business, and reallocation of capital and cash flow buys you time to focus on what will truly impact growth and profits going forward. If you focus on the falling revenues and falling profits to start, similar to selling out when the stock market falls down, you run the risk of losing out in recovery by investing your money in the wrong places and/or cutting expenses to early.

- Step Six: Implementation. The final step is to review and summarize your findings, and then enact your changes with the plan you’ve developed. With that, I have observed business owners who foresee a crisis and are afraid to sound an alarm bell for fear they might be wrong. If there is ever a time you question your judgement on a crisis, it’s better to be overprepared and look foolish when it turns out to be nothing, than underprepared. Being underprepared is the greatest crisis of all—a leadership crisis.

Now that you’ve got your bearings on the six steps of crisis management, I want to walk you through each of them in-depth, so you fully understand how to move through each in your own advisory business to help you make decisions with the numbers.

Assessment Of The Crisis

In the current moment, advisors are finding themselves in two major crises. One is a health care crisis for employees because of the spread of COVID-19, and the other is a financial crisis for the business itself from the market volatility.

If you take the wrong steps in handling these two crises, in the future, you will be in a ‘brand crisis’ that will hurt your reputation and hurt your future growth, and you may also face a ‘culture crisis’ if you treat people poorly. That’s a lot of crises to navigate through.

What Herbers & Company is seeing across the industry is that most advisors are focused on the wrong crisis – they’re concerned about their numbers in response to the financial crisis. Everything from falling revenues, to fewer profits, to tighter cash flow, is occupying their time and business planning.

But the business’ potential financial crisis is secondary. The major risk to financial advisory firms right now is the healthcare crisis. What happens if your leaders and financial advisors get sick? What happens if you become incapable of serving your clients? What if someone in your culture gets sick and does not survive? I don’t want to be morbid about it, but the fact is that’s a real risk.

In a service-based business, if there is no one to serve the client, the long-term effect is much more catastrophic than a period of reduced revenues and profits.

SWOT Analysis Identifies Ways To Protect The Business’ Culture

For the uninitiated, SWOT stands for Strengths, Weaknesses, Opportunities, and Threats. Starting with your Strengths helps you gain confidence in your business, and considering weaknesses helps you gain focus on what you need to do immediately to fix any issue you have been avoiding. In other words, it would have been quite unfortunate if you didn’t take the advice of your compliance attorneys to update your continuity plan. That would be a major weakness you need to solve today.

Opportunities are a bit harder in this crisis; many have already passed because the crisis has already started. The firms who are ahead are the ones who took COVID-19 seriously early on, who foresaw the threats with the pandemic headlines coming out of China. Most of the opportunities in this crisis are now in client communication and digital client service modeling, along with innovation.

As for threats, in COVID-19, the biggest threat to advisory firms, or any service-based business, is losing their culture. In this crisis, you have to know where to put your financial focus before you can ever deal with the numbers. A SWOT analysis helps you focus on capital allocation and where you need resources, and helps you determine what strategic goals you need to delay or accelerate.

If I haven’t repeated this enough, the biggest threat to advisory firms is the possibility of losing their people—either through illness, layoffs, or their own resignation resulting from how they see their leaders unsuccessfully (or unsatisfactorily) leading through this crisis. We are already starting to see financial advisors looking for new jobs due to the leadership issues. If your people are made to feel expendable by leadership now, then they’ll be looking for new opportunities when the crisis is over. As one crisis ends, another (self-inflicted) one will begin.

So, to begin, you have to understand that in the COVID-19 crisis, unlike 2008-2009 or other crisis we have gone through, employees and payroll matter most. Cutting people is the last place you should look to cut costs.

Continuity Planning And The Importance Of Flexible Compensation Structures

The unfortunate thing about many continuity plans in advisory firms today is they rarely are examined by human capital consultants (as we do for advisors at Herbers & Company). In a professional services business, where the chance of rapidly falling revenues may result in losing people from a crisis about people, you need to have the flexibility to make changes to compensation structures immediately.

I will not get into specific structures and details of how these compensation programs are designed because compensation programs are unique to every firm and how they operate. Compensation, as a general matter, changes behavior in advisory firms. If structured incorrectly, it can create yet another crisis (of compensation) resulting in high management of people and partners and/or turnover.

In general, though, if your advisors and partners are paid a salary, you need to make sure there is also a variable component of financial advisor and partnership compensation, so that if the revenue and/or profit falls below a threshold, these variable-compensation programs can be stopped during a crisis. Then, when you test a continuity plan, you assume the threshold is hit and a letter is delivered to every person affected, letting them know variable pay programs have been frozen. (If you have 100% variable pay, which is a compensation method rarely used anymore in independent advisory firms, this is a non-issue, as compensation naturally scales down when revenue declines.)

We have seen much success with these variable-pay programs in times of crisis because the employees, who’ve been through a continuity test or two, already know they’re coming. There are few shockwaves and rarely are there layoffs. When done right, your employee cost (i.e., gross profit margin) will rise and fall with revenues and the market cycles on Assets Under Management (AUM) pricing, preserving your culture until you have had time to adjust the rest of the business numbers.

At the very least, shareholders need to understand that their shareholder dividend can rise and fall, and to know the boundaries. Many firms make the grave mistake of flatlining shareholder dividends, and promising a fixed $X be paid out each month or quarter. This is a mistake in business management (and many of the reasons why people don’t want partners, and/or why partnerships often fall apart during a crisis), because partnership dividends need to be reinvented to recover.

If your continuity plan doesn’t outline changes in compensation and partnership pay structures that you would deploy as part of your continuity plan, my first recommendation—before you start cutting expenses and people—is to have an expert consultant and lawyer work together to help you design and implement those as part of your continuity plan and to keep updating it as this crisis unfolds. No different than clients needing financial advisors, advisors can gain new perspectives from working together with professional legal and consulting partners. In my experience going through this, the lawyer doesn’t know all the options for compensation, and the human capital consultant doesn’t know all the options to stay compliant. The bigger point is, none of us knows all the options. And neither do you.

What Herbers & Company knows is that if you build compensation programs within continuity plans, you will rarely, if ever, have to go through layoffs in your company in crisis. The continuity plan alone can preserve your people in a crisis through variable pay programs with thresholds, and significantly change the numbers automatically as you move through the crisis. When you run a test on continuity and send the letter about compensation changes in the test, you prevent the shock waves of compensation changes. In doing so, you ensure you hold together your culture and continue serving your clients when your clients need served the most.

Stabilizing Culture And Operations, And Using The Right Financial Stress Tests To Measure Stability

Once you know your people are safe (and they know it as well), the next step is to run financial stress tests on your firm to see how stable you really are. This is where I would recommend most financial advisory firms start right now.

There are three types of financial stress tests Herbers & Company recommends and runs on an advisory business. They are what we call aspirational, functional, and stability stress tests.

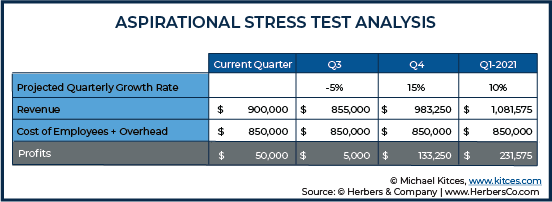

Aspirational Stress Tests

We’ll begin with an aspirational stress test, which is a financial stress test projecting out where you want your business to be X number of quarters from now. In other words, what decisions do you need to make today to impact where your business will end up in the long-term?

An aspirational stress test is about focusing on your firm’s vision and showing that you can sustain more hits and successfully recover from them afterwards. It’s not about the pain you may be currently going through.

If your vision is to expand the number of clients you work with, then you’d focus on growth in revenues, small wins in the growth rate as you sustain additional hits. Sequentially, these financial stress tests are done first when ordering the three types of stress tests, because they are designed to give you and your people hope through a crisis in the long-term.

Stress tests are difficult to illustrate because they are often detailed financial spreadsheets and integrated business strategies based on past performance and future bets. But, let’s say your vision is adding only a few client referrals to make up for the losses, knowing you’ve gotten X number per month in the past, while not cutting expenses (or at least not adding more expenses to the business).

An oversimplified example of an aspirational stress test is the following, showing another growth hit in the coming quarter and then allowing the crisis to play out until over. The following would be an example:

But here’s the hard truth: We don’t know when this current crisis is going to end, so these types of stress tests don’t hold much value for advisory firms because past performance is certainly no indication of future performance, especially in light of the dramatic culture shift. In an ongoing crisis, it’s hard to predict what past performance can tell us, therefore it’s nearly impossible to be aspirational.

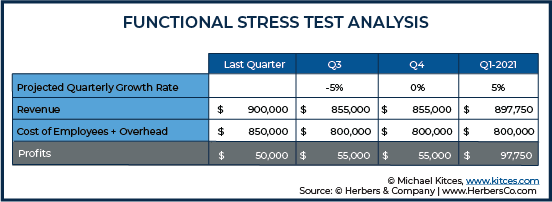

Functional Stress Tests

The second type, a functional stress test, deals with short-term revenue projections and profit margins. In other words, if you did something today to impact revenue (i.e., new growth ideas to make up lost revenue) what should that action be?

On the other side of this analysis sit your expenses. What expenses can you cut to give short-term relief and stretch your profit margins?

Most businesses are performing functional stress tests right now due to our economic situation. They’re asking themselves questions like these: Should I do layoffs? How can I cut expenses? What marketing programs do I invest in? How can I get new clients to make up for losses in revenue?

But here’s the hard truth about this crisis: There’s nothing to indicate anything about whether it will be (only) short-term – we simply don’t know when this crisis is going to end. And when you are in a crisis that is ongoing, investing in growth is risky business. Those who’ve done it and won often just got lucky the crisis ended when it did, and usually they are wildly innovative.

Growth programs in today’s environment are like putting up a billboard to advertise while a hurricane is passing through. What do you think the billboard is going to do?

The only thing advisory firms can really do with a functional stress test is cut expenses and increase client service hoping it results in referrals. But if you cut too many expenses you may not have the ability to serve growth after the crisis is over and may end up spending even more money to rebuild what you torn down during the crisis. Like the aspirational stress test, functional stress tests won’t provide much value or purpose right now, in our time of crisis, especially if you want to grow after it’s over. But it can help the firm at least get grounded in its current financial reality.

Using the same assumptions as the aspirational stress test above, and cutting $50K of expenses by laying off your associate advisor, an oversimplified functional stress test would be the following:

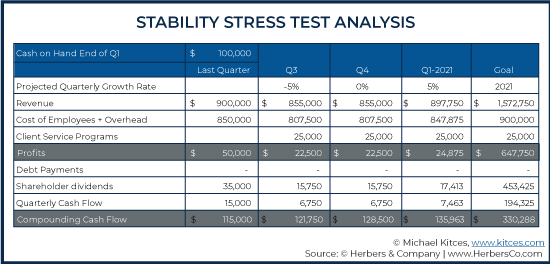

Stability Stress Tests

When you’re in a major crisis, your firm needs to operate differently than under normal circumstances. The stability stress test forces you to focus on capital allocation and cash flow – the core of any great business.

A stability stress test answers two critical questions: How far can we go by reallocating capital without making any major (adverse) changes to our culture that hurt future growth potential? And what can we innovate today that will slingshot our growth once this crisis is over?

The best bet to finding these answers is to look internally. They are found in your client service experience. They are found in how you serve your clients through this crisis. And, to serve them very well, you must have great people.

While functional stress testing might focus on doubling down on marketing efforts and cutting expenses, stability testing focuses on innovation, ownership, dividends, and debt payments using the balance sheet to run cash flowing modeling.

So, again, an oversimplified example might be the following:

Let’s say you had $100K cash in the business at the end of Q1 2020 and you didn’t cut any expenses at all. Your business continued to take short-term hits to the growth rate, like the stock market. And instead of cutting any expenses, the shareholders together decided to ride it out on cash flow.

Then together the shareholders ‘only’ took out of the business 70% of the profits last quarter, and decided to get ahead of the crisis by investing an additional $25,000 per quarter in Q3 and beyond on expanding client service programs and operations to make them more efficient and/or innovating in client service.

Herbers & Company knows that investments in client service programs pay off between seven and nine times on revenues within nine to twelve months when your focus is on organic growth. So, somewhere around Q2 2021, when maybe we have a promising vaccine almost done with clinical trials, you will start to see the growth rate turn positive. Usually, it will turn fast on new client referrals if you make investments in your business on client service.

In doing all this, often what happens is you will see your growth rate continue to fall (if the market isn’t giving you any wind in your sail) and your profit margin will go down as well. But your compounding cash balance will grow (as your profit margin is still positive, buffered by prudent cost cutting).

If you do it right, sometime twelve months from now all the key performance indicators (KPIs) in your business will be positioned to take off together. You will have the potential to see rising growth rates, rising profit margins, rising cash in the bank and increasing valuation until you hit another growth barrier (or crisis).

Here’s what a stability stress test (with goals incorporated into it) looks like with the primary focus on growing cash in the business bank account and innovating client service and operations, with an illustration that your investment in the business of $75,000 for client service over the past three quarters (Q1 2021, Q4 2020, and Q3 2020) repaid you nine times on revenue in 2021:

The real question when running stability stress tests is: are you willing to invest in your own business in a downturn, like you would invest in the market? I would.

The Importance of Strategic Planning

Over the past six months, my consulting team at Herbers & Company has run over 260 stability tests for advisory firms. Based on our findings from those tests, here are the nine places you should look to fix the problems your firm is likely experiencing right now and will experience in the future.

I would begin going through the following steps with your numbers, in this order.

- Refinance the debt you carry to lower rates. We recommend you do this with a reputable bank, and not take outside capital infusions. Unfortunately, there are some organizations and capital institutions taking advantage of advisory firms and offering capital that looks a lot like mezzanine loans when deconstructed. In other words, non-banking institutions may offer variable repayment terms, such as requiring a percentage of revenues until the loan is paid back, which makes the interest rate on them very high as you grow. If you cannot pay them back, they can take equity, but that can be devastating to an advisory firm that isn’t ready for having outside investors at the table. The safest bet when refinancing debt is to work with a bank. I also suggest that you review all debt proposals with a third party who is not conflicted.

- Reorganize ownership, partnerships, and/or your own compensation structure. In other words, start with cutting expenses at home. Shareholder dividends and partnership structures in most advisory firms are the biggest ongoing problem in the current environment. Reorganizing and redeveloping your partnership programs, incentive structures, and shareholder dividends is critical. Often we will not cut shareholder salary; instead, any dividend payout on the profit margin is often reduced or restructured. These tend to be variable payout structures on the profit margin that have thresholds if the profit falls below a certain percentage (as covered above). In doing this, you will free up some capital for partners to reinvest back into the business on client service. The goal is for those reinvestments to pay off in 2021. If there are new business development incentive structures, ideally we’d want to keep those working as normal.

- Lift the (profit margin) exceptions. For reasons I don’t understand, many advisory firms run their firms to ensure a certain profit margin. In other words, firms don’t allow the profit margin to dip below 15% and/or 20% or whatever. In normal times, if this is how you want to run your business, fine. In today’s time, you need to focus on the cash flow more than anything else. If profit margin has to dip to maintain healthy cash flow in the long-term, it’s far better to preserve the future than maintain the rules of the past.

- Eliminate travel and expenses. Travel and entertainment are automatically slowing down for all of us right now; make sure you make intentional adjustments to your projected expenses based on this slowdown. As more and more conferences are transitioned to virtual, there are more and more options for you and your employees to earn your required CE online/virtually.

- Trim the fat in overhead. Take a good hard look at what’s working and what isn’t working in your operations. Notably, identify if you’re paying for technology you aren’t really using. There may be marketing programs you can recalibrate to lower cost solutions that get the same result, or client experience processes that can be innovated. Herbers & Company often tells clients, “…use your brain, not your pocket book…” It’s especially true right now. Creative innovation and recalibration as this crisis in paramount. Your goal is to be ready when it’s over.

- Stay home. Trim your rent and office expenses. In a virtual environment, you have an opportunity to move to slimmer phone systems and communication methods. While I hope you don’t default on anything, in this crisis, it’s better to default on rent before cutting a person from your team. With our profound culture change with COVID-19, one must wonder how important commercial real estate is going to be after this is over.

- Look at employee benefits. Have your employee benefits gotten out of hand by offering too much? Financial advisory firm owners tend to be quite generous paying for internet at home, cell phones, wellness programs, memberships to associations, conferences for continuing education, additional degrees and designations, etc. Putting lower limits on these benefits and having all employees make small benefit cuts together is far better than layoffs. In the good times, these are welcome benefits, but employees respond much better to cuts in their benefits than to cuts in their compensation in a crisis.

- Strip out extras in your client service, expand communication and innovate. If you hold events or create experiential moments for clients that require additional branding and design, you can trim those services that go above and beyond from your client experience process until your firm returns to more stable ground. Take a hard look at your client experience process and determine if there are ways to do it better and more efficiently. Often times, you’ll find there are areas you can improve such as how the sales process is conducted.

- Look at your people last. The best way to grow in hard times is to serve your clients really well. Without a confident and stable team surrounding you, your service (and your client relationships) will suffer. Cutting your team in this crisis is a brutal mistake. Make it your last resort. In general, we don’t recommend making small base salary compensation cuts for all employees across the board in times of crisis. Doing this in a crisis almost always guarantees the employee(s) will leave after the crisis is over.

If a variable compensation program was in place before the crisis, this problem would solve itself. If you are overstaffed, you likely may need to do some layoffs because the investment is not likely going to return in the short-term, assuming you are not willing to ride out the crisis on cash flow and/or your firm was not properly liquidated to carry the investment in talent through a hard time.

On the other hand, if you have been holding onto people who really should have been let go prior to the crisis, my hope is you will learn to let go faster in the future. At any time, your business can go through a crisis and if you hold onto people who really should not be there, you carry the responsibility for those employees not being able to have a more optimal time to find a new job.

Implementation

Advisory firms will get through this crisis by focusing on three things: your culture, your clients, and the stabilization of your organization.

Of those three aspects of business, advisory leaders struggle most with stabilization. The very nature of a financial advisor is technical planning, but today, in the wake of COVID-19, the plan is to stay steady and be creative when there is no plan to follow. In the end, my hope is all advisory firm leaders will focus on client service and operations while expanding their leadership education and learning more. If you do, you will come out of this moment stronger and more equipped to confront the next crisis, whenever it comes along, with capital you saved throughout and a strong cash flow.

And, if you are creative, you’ll grow through innovation you invest in now, after the crisis is over.

Leave a Reply