Since the audience for this article comprises accountants, let’s start with a number: 35%.

What is that? It is the percentage of organizations in the United States that have “a formalized succession planning process.” Meaning just a little over one-third of U.S. businesses are prepared for the multitude of forces that can trigger the need for a succession, from something as dramatic as an owner’s death to an unexpected exodus of top talent.

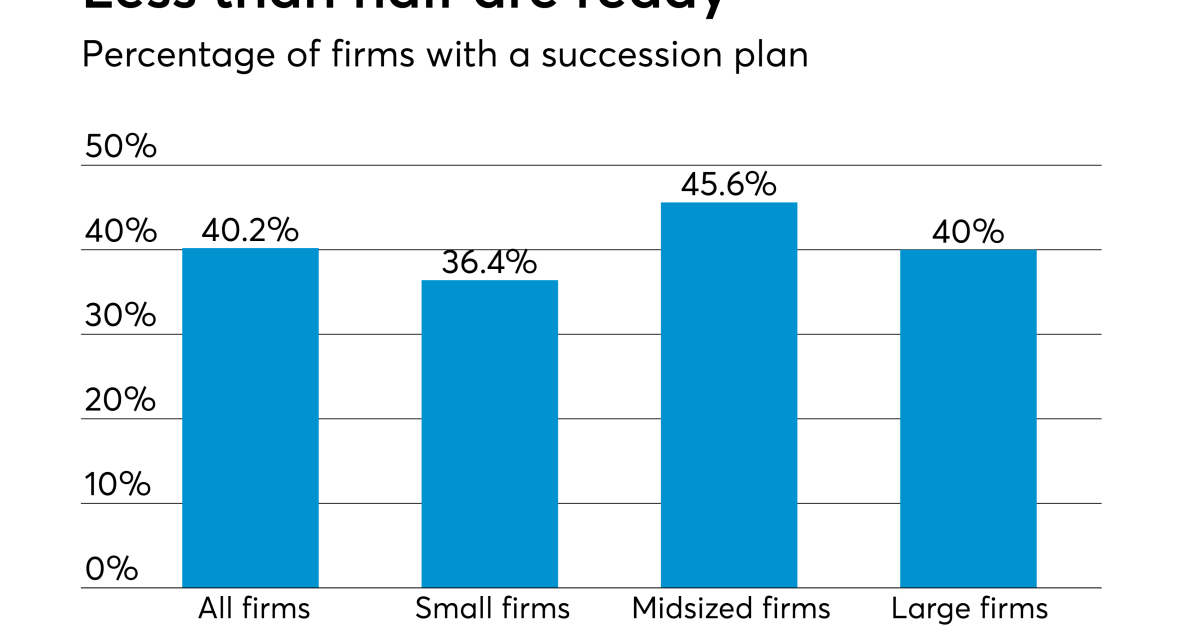

One more stat: less than 50%.

That, according to AICPA, is the percentage of all accounting firms that have succession plans in place. So, our profession is doing a bit better on the succession front than the general business population, but maybe not when you consider another AICPA stat: 80%.

That is the percentage of accounting firms that “expect succession planning challenges in the next five years.” How important an issue is this for our profession? Important enough for our association to do an ongoing survey on “CPA Firm Succession Management,” and produce an accompanying “Multi-Owner Survey Report” some 40 pages long.

Multiple sources addressing succession planning point to a new urgency regarding the process. For one, count on an unprecedented number of exits of high- and top-level business leaders from all disciplines, including accounting. Consider the fact that 10,000 Baby Boomers reach retirement age every day.

Take a look around your own firm (and also look in the mirror) to see if an uncomfortable number of senior staff are on the cusp of retirement. Who will replace them? The time to figure that out is not at their going away party, but now.

If you talk to people in accounting about the necessity of having a succession plan, few would disagree. In fact, many of us probably encourage our clients to produce one. So, it is a bit startling when you find out that over half of us don’t have one. But here’s some good news from the AICPA survey: 60% of respondents either plan to start the succession planning process in the next year or two, or have started the process and will soon complete it.

Like any process, succession planning has multiple steps. Step one, for owners and senior staff alike, would be to acknowledge that, at some point, and maybe sooner than they think, some form of succession will occur. And then to talk about it.That may seem like an oversimplification, but for many firms, particularly those with founders at the helm, broaching the topic of succession is difficult.

For founders, this is literally “their baby” that they created and nurtured and made successful. Talk of leaving its fate in the hands of other people proves difficult. But those conversations must be had. Why? The AICPA report offers a very elegant answer: “Succession planning gives firms the power to set the tone and direction with which they wish to send the firm into the future.”

Stubbornly refusing to plan a succession will see your firm sent into the future haphazardly, perhaps with a fair share of infighting, thereby jeopardizing the firm itself, and its employees and clients, and perhaps ensuring you will leave no legacy because your “baby” will disappear altogether.

In terms of the “nuts and bolts” of succession planning, tutorials abound, as do firms that specialize in helping the planning process. But step two needs to be determining what succession looks like at your firm. There are basically two approaches: internal and external.

An internal succession plan grooms current employees through training and education and experience to become those who will captain the firm into the future. An external succession plan, as its name implies, agrees that the best course for the firm, employees and clients is to seek talent outside the firm to fill the key positions that will keep the firm solid and whole after the exit of a founder and/or senior staff. But if there is one succession note that is sounded over and over again, it is this: Do not wait until the firm is on the cusp of a succession.

Whatever the founder’s age, or that of partners and other top management, “make believe” if you will that succession could occur tomorrow. Why? Because it could. And that includes creating a succession scenario for the very real possibility of a merger, which can create a whole other element of succession.

If we remember that the root word of “succession” is “success,” a larger firm in a merger will be evaluating new talent from the merged company, and it should also have a “success” plan to develop that talent. And I, Wendy, am happy to report, that is what happened for me. The merger four years ago of the firm for which I worked with Prager Metis triggered an awakening of talents untapped in the culture of a smaller company.

It comes down to this: Charles Darwin said, “People keep calling my theory ‘survival of the fittest’ when really it is survival of the most adaptable.” Despite even careful succession planning, or a new company that is welcoming, change is often hard. And if you are an employee, at whatever level, in the midst of a succession, or with one on the horizon, keep Darwin’s quote in mind. Go all in, and see this as an opportunity. If you see succession as a chance to grow, you might be pleasantly surprised at what the unknown can bring.

Leave a Reply